The definition of tax efficient withdrawals in retirement means correctly managing which account type your investments are in, when to pull from these accounts, and whether you should convert some of your tax-deferred accounts to Roth IRAs to reduce your overall tax burden.

Making tax efficient withdrawals after you have retired comes down to the differences between how each account type is taxed. Here are the 3 account types in terms of tax treatments.

A taxable account – This includes bank accounts and brokerage accounts. With these taxable accounts, you pay taxes every year on the dividends and capital gains produced by the holdings, even if you don’t actually sell anything in the account. If you own mutual funds or ETFs, the fund manager is buying and selling shares to adjust the fund’s holdings. You are taxed when the manager sells a stock for a gain. You are also taxed when a stock within a fund pays out their quarterly or annual dividend. If you earn any interest on a bank account, you are taxed each year.

The second account type is tax-deferred accounts like 401(k)s and IRAs. These accounts are only taxed when you take your money out. You are taxed at whatever your tax rate is at that time. Unlike the brokerage account, you do not pay taxes each and every year. When a capital gain or dividend is paid out from a mutual fund or ETF, you can reinvest 100% of the payout into buying additional shares rather than into paying taxes.

Roth IRAs – These accounts are the most tax-efficient. You pay taxes up front, before contributing to these account types, and you (or your heirs) never pay taxes again. There are no ongoing annual taxes like a brokerage account and there are no taxes upon withdrawing like a traditional IRA or 401(k).

Each of these account types has their own set of rules. By using the rules wisely, you can optimize how much of your money you keep and reduce the amount you give to the government.

Creating a strategy that follows the rules correctly and maximizes your money requires some expertise. To talk with us about your situation, please schedule a free, first meeting using this link.

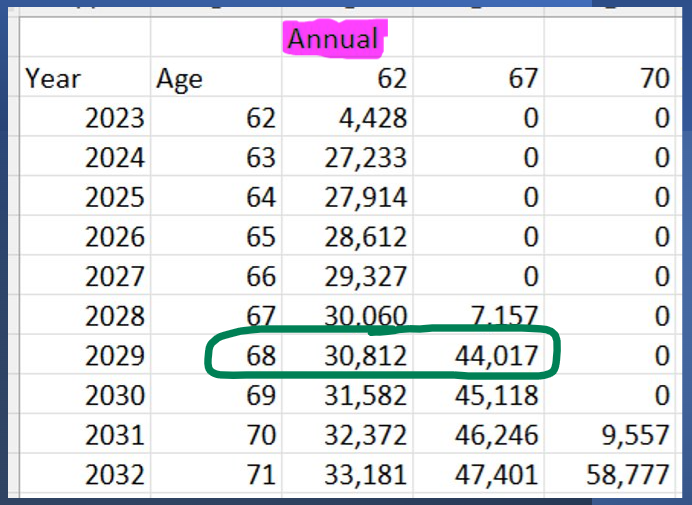

You’ve probably heard or read that you should wait until age 70 before claiming Social Security. In this blog, I’m going to show you actual numbers, so that you can see just how much of a difference delaying Social Security can make.

The details of our scenario are Diane is turning 62 in November and retiring. She is single and has never been married. This keeps the scenario simple because there are no spousal benefits involved. Her Social Security full retirement age benefit is $3,163 per month at age 67. To get that large of a Social Security benefit means that she has been a high-income earner for many years. I am going to show you how much she will receive if she claims at age 62, 67, and 70.

The following spreadsheet shows the annual amounts under different claiming ages.

If she claims at 62, in her first full year of benefits she will receive $27,233. That amount with cost-of-living increases (which are assumed to be 3% per year) increases to become $30,812 per year by age 68.

If she delayed claiming to 67, instead of receiving $30,812, she would receive $44,017 that same year.

That’s a big difference!

Continue down to the bottom row and look at the year she turns 71.

If she claims that 62, she’ll be receiving $33,181 per year. If she claimed that 67, she would receive $47,401 per year while claiming at 70, she would receive $58,777 per year. That’s a significant difference!

Can she afford to wait?

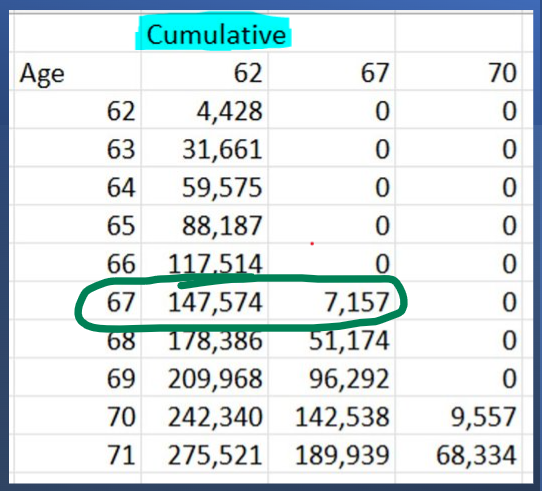

If Diane is going to wait until age 67 to claim Social Security, she must have money set aside or other income to live on. This next spreadsheet shows that she would have received $140,000 by the time she is 67. This was calculated by adding up the benefits received each year.

If she does not have a way to pay $140,000 of bills, then waiting is not even an option. She has to claim early.

If she does have money set aside in a bank account or in a brokerage account, then she can afford to wait to claim her Social Security. Most often the breakeven point comes around age 79 years’ old.

So, if Diane is going to live past age 79, she should delay her Social Security benefits.

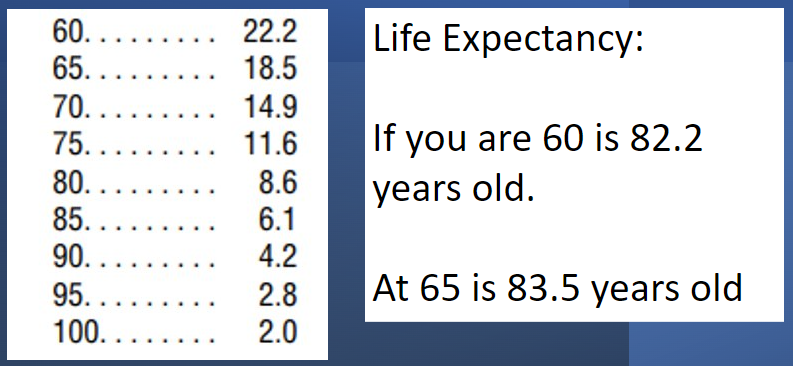

Life Expectancy

If age 79 sounds like old age that you’re unlikely to reach, well life expectancy tells us that half the population who are currently 60 are going to live past age 82.2. The odds of living into your 80s are even better if you’re already 65.

Cost of Living Adjustment (COLA)

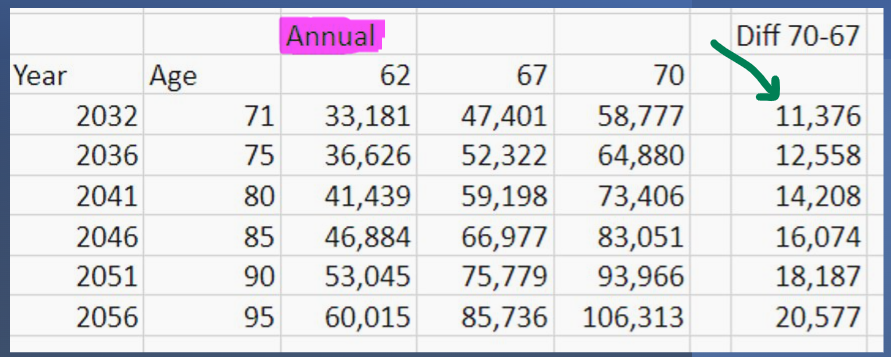

Another thing I want to point out about Social Security benefits and the advantage of waiting to claim is that the difference increases each year as you can see on the right-hand column of the following spreadsheet. The reason the benefit difference increases each year is that Social Security gives a COLA. A cost-of-living increase that’s a percentage amount.

A 3% increase on $58,000 is larger than the 3% increase on $47,000. Over time the COLA increase compounds, so that the difference is increasing for each year that you stay alive.

If we look at the age 90 row, we can really see how big of a difference waiting to claim Social Security makes if one lives a long life.

In this example, claiming at the various ages would be $53,045 versus $75,779 versus $93,966. That’s a really big difference!

I recently spent four days at a tax training seminar for financial advisors. There were many impactful topics covered in the lessons. One of those, which I will cover in this blog post, is referred to as the widow’s (or widower’s) penalty.

When one spouse dies, the remaining spouse is allowed to file their taxes as married filing jointly (MFJ) one final time in the year of their wife’s or husband’s death. In the following years, unless they remarry, they must file their taxes as single.

This shift from married filing jointly to single can create a large tax increase, even though the widow’s / widower’s income goes down in a lot of cases. Let’s look at an example.

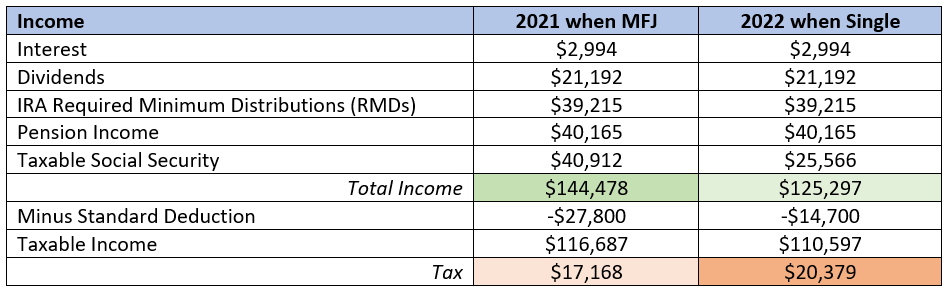

In this example, the couple were both retired and had various income streams. They had interest and dividends from their investments, required minimum distributions from their IRAs, a pension, and two Social Security benefits.

After the husband’s death, the widow’s Social Security income goes down because the survivor only gets the larger benefit, not both. In this example I held RMD and pension income constant for simplicity’s sake. In reality, the RMDs would change from year to year, but the pension income could stay the same if the pension had a 100% survivor benefit.

The following table shows the various incomes and the tax due.

You can see in this example that the widow’s income dropped $19,181 from $144,478 to $125,297. However, her taxes increased by $3,211 (from $17,168 to $20,379)! This is the widow’s penalty.

What can we do about this?

Planning for this scenario should be done many years in advance. If we look at the main sources of income, their pension income and Social Security income are out of our control. They will be what they will be. It is the IRA required minimum distributions (RMDs) that we could make an impact on, depending on the strategies we implement and their timing.

Large IRAs are a good thing to have, but they can create tax issues if they are not withdrawn from in a smart manner. It all depends on your particular circumstances and numbers, but perhaps using the IRA money to live on when you first retire, before RMDs begin would help to minimize these taxes. Or perhaps an aggressive Roth conversion strategy early in retirement would be the best option for you. There are no hard and fast rules, it all depends on how the numbers work out.

Medicare Impact

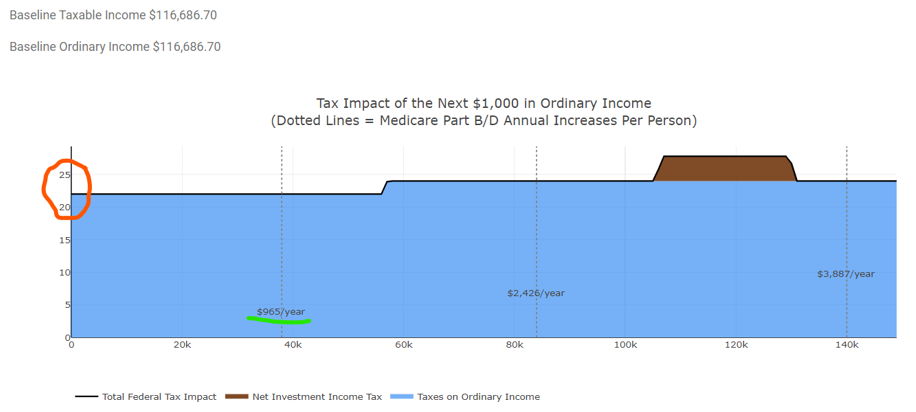

The next two diagrams bring up another important consequence of not optimizing your withdrawal strategy. These diagrams show the tax implications of each additional $1,000 of taxable income. In the top one, the married couple has about $38,000 of additional income they can handle before their Medicare premiums are bumped up due to passing an income limit. The increased Medicare expense is shown as the dashed, vertical lines.

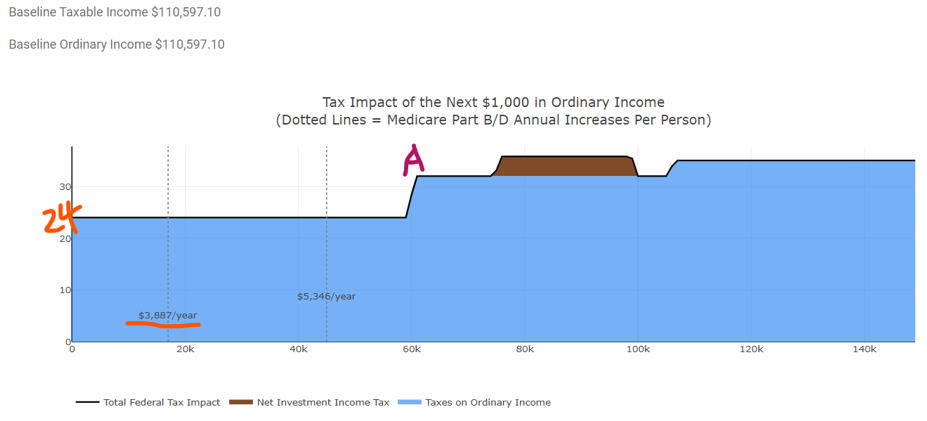

In the single widow’s graph, the second one, she only has about $17,000 of additional income available before her income pushes up her Medicare premiums.

The issue is not just that the widow will reach the Medicare expense threshold sooner, it’s that the increase will be far more significant than the couple who are both still alive. The widow would have to pay $3,887/year more for Medicare versus $965/year more for the couple.

If her IRA investment value stays about the same size or increases, her RMDs will be increasing each year, and she will likely hit this Medicare barrier, increasing her annual expenses by $3,887/year.

You can also see that in the second diagram showing the widow’s taxes, she could reach the 32% Federal tax bracket with $61,000 of additional income (point “A” on diagram). Whereas the 32% bracket does not show for the MFJ couple, even with an additional $150,000 of income.

Having a plan in place to manage the widow’s penalty tax issue, and other issues that are out there, could save you or your spouse a large amount of money. If you are interested in discussing your withdrawal plan, please use this link to set up an appointment.

Looking for something good to take away from the forced economic shutdown from Coronavirus-19?

Although the shutdown crimped our lifestyle, it has had the benefit of forcing us to discover our minimal required spending. No travel, no eating out, no shopping, and no activities with friends leaves only necessities to spend money on.

Knowing how much you pay each month for necessities, or your minimal required lifestyle, is a required step to creating a safety-first retirement.

In a safety-first retirement, you cover your necessary expenses with guaranteed income. You don’t rely on the stock market for even $1 of your essentials. The benefit is stress-free living.

Safety-first retirement income sources include Social Security, pensions, annuities, bonds, and cash reserves.

Imagine how stress-free you would have been this year if you had guaranteed income arriving in your checking account every month before, during and after the coronavirus lockdown.

Calculating Your Definition

In normal times it’s very hard to calculate what your essential spending would be because it’s hard to say whether things are needs or wants. Coronavirus however has limited us and created the perfect scenario for us to learn what our needs really are.

We all have different definitions of needs / minimal lifestyle / essential spending. That’s fine, but now you can easily calculate what yours is.

If you look at your average spending in March through June, subtract out any large expenses you had like home improvements, and that average spending is your essential spending. That’s as simple as it will ever be.

Once you know that number, we can investigate safe methods to generate that level of income.

More about Safety-first

This idea of a safety-first retirement is catching on in the financial planning community.

According to safety-first, the objective for retirement is first to build a safe and secure income floor for the entire retirement planning horizon… Once there is enough flooring in place, retirees can focus on upside potential with remaining assets.

Since this extra spending (such as for nice restaurants, extra vacations, etc.) is discretionary, it will not be the end of the world if it must be reduced at some point. The protected income floor is still in place to meet basic needs no matter what happens in the financial markets.

Stated again, the objective of investing in retirement is not to maximize risk adjusted returns, but first to ensure that basics will be covered in any market environment and then to invest for additional upside. [These italicized quotes come from the book titled Safety-First Retirement Planning: An Integrated Approach for a Worry-free Retirement by Wade Pfau.]

With your essential expenses covered, you know you can live a basic lifestyle (like during coronavirus), no matter what happens. If the stock market continues to do well, then you will have money to spend on fun and luxuries.

Why safety-first is a new idea

Financial advisors have generally been recommending clients hold stocks and bonds in retirement and withdraw 4% or less every year. The reason this has been the standard is that most advisors get paid based on the size of their client’s investment accounts. They charge AUM fees.

Safety-first is catching on with advisors like myself who do not rely on investment AUM fees. Andrew Marshall Financial, LLC does not suffer the conflict of interest of losing AUM when recommending you use a lump-sum of your investments to buy an immediate annuity were it the best solution for you. Furthermore, we receive no commission or kickback if you purchase an annuity.

Issues with using safety-first

The difficulty with using this strategy is getting over the fact that it usually requires handing over a large portion of your retirement savings to an insurance company to purchase an immediate annuity. (Pensioners are usually able to achieve a safety-first retirement without purchasing an annuity, but not always.)

A lot of people like the feeling of control from having their investments in an account that they can see and adjust. However, it is important to remember that when you purchase an annuity, you haven’t given up your lump-sum with nothing in return. You have guaranteed yourself food, clothing, and shelter for the remainder of you and your spouse’s lives.

Why it Works

When you purchase an annuity, you are pooling your money with all the other individuals who have purchased that annuity. The insurance company becomes responsible for your retirement investments rather than you.

By pooling your assets with other people, it becomes easier to fund everyone’s goals. If you fund your own retirement, you need to be cautious because you or your spouse may live well into your 100s. Take out too much and you could go bankrupt before then.

When you are part of a pool, the payout can be higher than the recommended 4% for self-funding because not everyone will live into their 100s. In fact, some people will die young. Their investment remains in the pool and is then spread among the remaining annuitants. Currently, a single woman in California aged 65 can receive a 5.3% payout on her purchase amount.

By pooling your resources, you accomplish the actual goal of your many years of investing; providing income that lasts your entire lifetime.

If a safety-first retirement plan sounds intriguing to you, or you worry about how you will cover your retirement spending needs, then please contact us to set up a call.

This post is a reprint of our newsletter sent to subscribers in June 2020.

Stockmarket

When the next massive event threatens the stock market, you should feel some comfort knowing that the government will step in and do everything it can to keep the stock market up. After all, our capitalistic society relies on the stock market.

Every working person’s retirement account, every insurance company, and every pension fund depend upon the stock market maintaining a certain level. Without the stock market, investments in new companies and ideas would not happen.

If the stock market were to collapse and not recover, there would be far worse rioting in the streets than we are seeing now.

The government (by which I mean the Federal Reserve and / or Congress) may not get the recovery right first try, or it may take them longer than is comfortable, but eventually they get there. The fact that this shut down caused market reactions similar in many ways to the 2008 crisis meant the government knew what to do and was able to step in quickly.

The Federal Reserve’s credibility has gone a long way towards calming these markets. Their forward guidance (what they say they will do in the future, even if they don’t really do it) was convincing enough to the big money managers, and they have responded the way the Fed hoped they would.

Bond markets are working again, and the stock market has recovered.

How do we apply this? You should be comfortable owning stocks. Stocks are a long-term investment and have always bounced back. Review your asset allocation if you were nervous in March when the stock market was falling fast, but by all means continue to own stocks.

From an economic standpoint, we are in a similar situation to 2009. From 2009 until the emergence of the corona virus in 2020, the stock market had its longest bull market run in history. That history could repeat as stocks will again attract more investment than low yielding bonds.

Bonds

The Federal Reserve has said it will enter the bond market to keep interest rates low. Let me explain how this works.

Bond interest rates and prices move in opposite directions. For me, it is easier to think through the price side first since price movements are the same regardless of what item people are buying.

Let’s take a real estate example. If several couples are trying to buy houses, then to ensure that one couple gets the house they want, they must pay a bit more than the other couples. If they do, prices are rising.

Bond prices work the same way. If more people are buying bonds, then in order to ensure they get the bonds they want, investors will have to pay a little more than the other buyers. Bond prices are going up in this case.

If the bond price is going up, then the interest rate will go down. This makes sense because if there are a lot of buyers, the issuer of the bond doesn’t need to give a high interest rate to entice the buyers who are already keen to buy.

This same scenario works in the reverse. If few people want to buy, price will go down, interest rates will be higher to entice more buyers. How is the Federal Reserve able to manipulate interest rates?

They have stated they want to keep interest rates low. To keep interest rates low, there need to be a lot of buyers of bonds. A lot of buyers mean high prices and low interest rates.

In this case, the Federal Reserve itself becomes “a lot of buyers”. They have unlimited money to buy, and can continue buying government bonds for years.

The Federal Reserve Chairperson, Jerome Powell, said on June 10th that they will be buying at least $80 billion of US Treasuries and $40 billion of mortgage backed bonds every month!

How do we apply this? Owning bonds for yield will be an impossible situation for at least several years. Investors will need to use a total return strategy, not choose investments based solely on their yield, and remember that the most important reason to own bonds is to offset stock losses.

Low interest rates make paying off your mortgage more attractive. Say you have a 3.5% mortgage. There is no bond investment available today, other than a high yield (read “risky bond” which you shouldn’t buy), that will give you anywhere near a 3.5% yield.

The Vanguard intermediate bond fund (VBILX) is yielding 2.38%, but you must pay taxes on that. The Vanguard tax-exempt California Muni bond fund (VCADX) has a distribution yield of 2.33% currently.

The average total return on 10-year US Treasuries for 2009 – 2019 was 2.94%. Paying extra towards the 3.5% mortgage looks better under today’s circumstances.

For retirees, buying an immediate annuity with the money you currently have allocated to bonds becomes more attractive. Immediate annuities do not have the fees of variable annuities and accomplish the goal of providing income for the rest of your lifetime.

It’s like buying an additional Social Security payment.

A joint immediate annuity for a 70-year-old couple currently pays 5.55%. Of that payment, only 14% is taxable.

Hopefully you and your family are healthy and doing well. If you want to schedule a meeting just email me at andrew@andrewmarshallfinancial.com.

I have been doing Zoom meetings and it is very convenient. I have found virtual meetings make it easier to help some clients because we can share screens, and I can talk them through how to buy/ sell shares, see what their accounts hold, and they can see me check or update their financial plans.

The following newsletter was originally sent to email subscribers on March 27, 2020. If you would like to receive my email newsletter once per quarter, please sign up here:

Congress Spends $2 Trillion. It Won’t be Enough.

Hello,

I hope you are all doing well, you and your family are healthy, and you are staying sane in these strange times. It has been difficult to believe the virus is as bad as we are told. Walking around Carlsbad, it seems like there is no reason for the isolation.

However, a college friend of mine’s father died of COVID-19 last week in Kansas. That along with the news coverage showing hospitals in Italy and Spain overloaded with patients make it seem a lot more real.

The number of new cases is rising here in San Diego county. It looks like a fairly steady rise and not an exponential rise at this point. Hopefully it doesn’t turn exponential.

The shutdown could continue for a lot longer than people are thinking. Wuhan has been shuttered since January and won’t be opening for another nine days. That same time frame puts us on lockdown until June 8th. The risk of having a relapse of the disease spreading will keep the lockdown policy in effect for longer than first anticipated.

Economically, things are going to get a lot worse from here. This week, 3.3 million people filed for unemployment benefits. No one is going back to work any time soon (apart from new hires at Amazon, Costco, and grocery workers). I expect the high unemployment numbers to continue. The slew of bad economic numbers that will be coming out in the next few months will trigger another round of stock selling, in my opinion. Until the trajectory of the virus is known and understood, the stock market will test the recent low. I think there will be opportunities to buy stocks in the future.

Longer term, this ordeal is going to exaggerate the wealth gap in America. The “little guy” will have a much more difficult time without earning income. I can see a lot of small businesses not reopening this summer when the lockdown is lifted.

What steps can you take now?

The stock market selloff opens opportunities for those with a long-term outlook. The amount of money governments around the world have put into the economy means the low bond yields forcing investment into stocks for returns will continue for many more years. It should be obvious that the government will do everything it can to keep the stock market going. Long-term that means you should continue to stay invested in stocks, even if it is scary at this time.

The next couple of months may be a good time to do a Roth conversion. Converting in a down market means you will get more shares for the same amount of money. If your income will be lower than expected this year, you may be able to convert a larger amount and stay within the same tax bracket.

Those who are taking required minimum distributions (RMDs) will not be required to take this year’s withdrawal. This exception is part of the CARES Act that Congress passed today. If you have enough to live on and don’t need to take your withdrawal, you should not take it this year. Leave the money in your account to grow tax deferred.

If you have Federal student loans, your interest will automatically be set to 0% for at least 60 days. If you do not want to make a payment during this time, you should contact your loan issuer and ask for a forbearance. Making a payment now means the entire amount will be applied to the principal, which will be helpful if you can afford the payment.

Now may be a good time to refinance your mortgage. There has been a lot of volatility in the mortgage market the past few weeks, but you may be able to get a good deal right now. If not, try again in a week. Things are moving that fast.

Now is also a good time to look at your estate plan. Make sure you have a Will, Power of Attorney for both healthcare and finances, and an Advance Healthcare Directive.

If you have concerns or would like me to assess your situation, please make an appointment.

LLiS.com Insurance Broker for Fee Only Financial Planners

In February, I attended two days of insurancetraining in Clearwater Beach, Florida. I don’t sell insurance, but part of creating a comprehensive financial plan is understanding ifclients are fully covered by their various policies.

Two training sessions were on long term care insurance policies (LTCi). I came away from the sessions with an understanding of the risk a couple is taking by going without long term care insurance and the tax benefits of owning a policy.

Risks of Not Owning LTCi

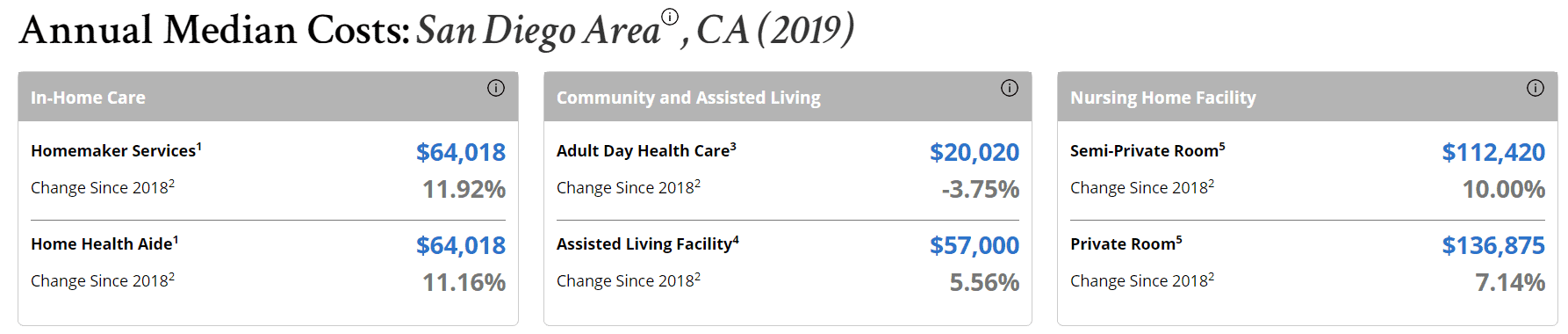

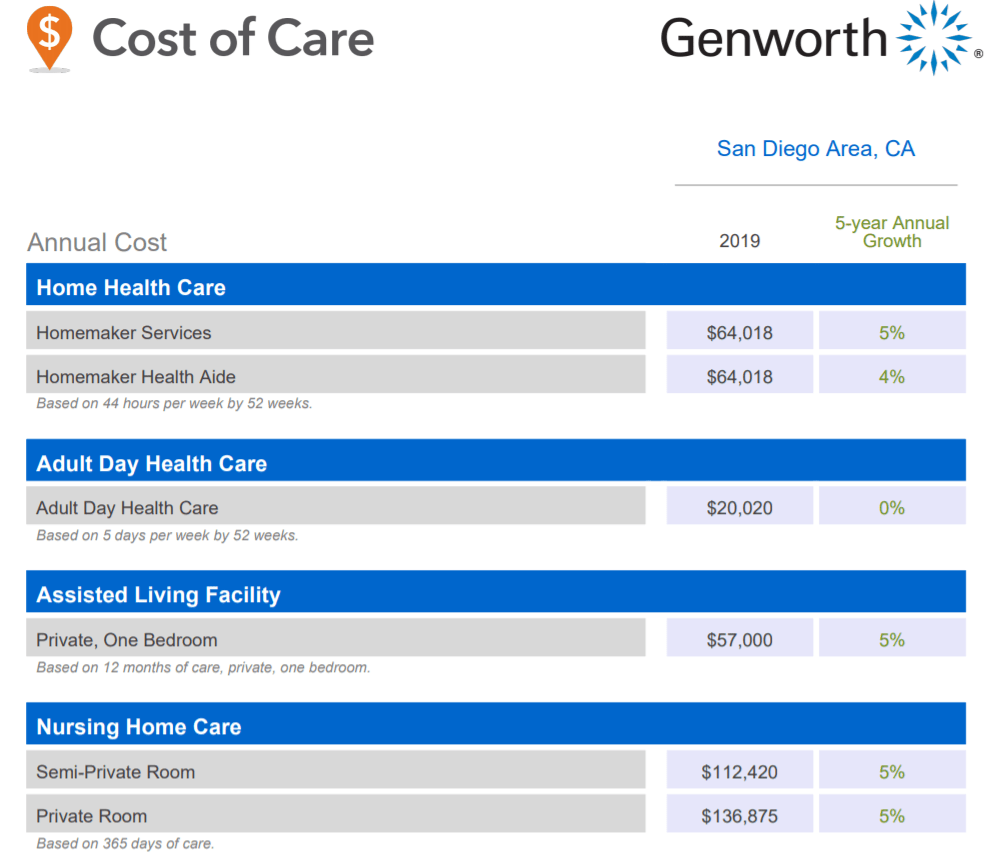

We all know that health care costs are increasing rapidly each yearas are long term care costs for all types of care: in-home, assisted living facilities, and nursing homes. The costs are shocking when you first hear them. Here is a link to a website that will show you an estimate for the price in your area of the country:Genworth Cost of Care Survey.

The general strategy that most retirees are using for LTCi is to wait and see. They plan to use their investment assets or their home equity to pay for anyassisted living ornursing home costs.

I have generally gone along with this idea but realize now that this will only work well under certain conditions. Those conditionsinclude having a sizeable net worth, when there are no goals for passing assets on to kids or charities, and when the long-term care is needed after one spouse has already passed away.

The big riskof not having LTCiis,how will the healthy spouse’s life change after paying for thelong term careneeds of their spouse?

Commonly, the healthy spouse will look after the ill spouse at home for as long as possible, but it eventually gets overwhelming. The physicality of transferring someone into and out of a shower or a bed is really hard work. The time and effort spent being a caregiver really depletes the caregiver’s quality of life. As the caregiving spouse gets older, the more likelya need to hire someone will arise.

If they use their investments or tap their home equity to pay for it, then the resources remaining for support of the healthy spouse’s life can get depleted quickly.This will leave the remaining spouse with a very different lifestyle than what they were used to or what they dreamed of as retirement living,before their spouse became sick or incapacitated.

Let’s look at some financials to see what the aftermath of a nursing home stay could be.

Long Term Care Costs for an Example Couple

The average time spent in a nursing home is 18 months. The median (or middle) time is 6 months. There are some really long stays that pull the average out.

Let’s look at an imaginary example and say the male of our married couple had a stroke and didn’t recover well. He had to be moved into a nursing home and was able to stay alive for two years thereafter.

The total cost for two years in a San Diego area nursing home is $273,750. If this couple uses their investments to pay for this nursing home, how much will itactually cost them?

By using their investments to pay for it, long term care needscouldactually become 20% to 50% more expensive. Why? Their taxrate.

Depending on the tax bracket and what type of account the investments are in, withdrawing to cover LTC expenses will create taxable transactions.

Best Account Types to Pay for Long Term Care

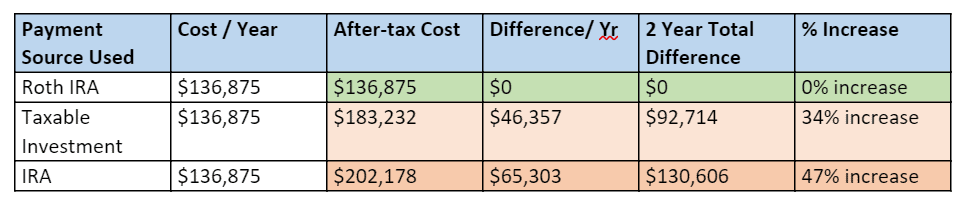

The best option is to use a Roth IRA account.There are no taxes due on a Roth IRAwithdrawal.

The next best option is to pay capital gains tax on withdrawals from a taxable investment account. This will most likely be taxed at a rate of 15% Federal, plus state taxes.

The costliestoption would be to pull from an IRAaccount. IRA withdrawals are taxed as ordinary income.

Chart of After-tax Long Term Care Costs

We will assume our example couple is in the 22% federal tax bracket. That corresponds to a 2020 annual taxable income level of $80,251 to $171,050. In this tax bracket, long-term capital gains would be taxed at 15%. For both types of taxable withdrawals, the California State income tax would be an additional 10.3%.

Cost of care per year: $136,875

This chart shows the dramatic increase in actual cost they would pay after tax for self-funding a nursing home stay. $202,178 versus $136, 875. A 47% increase on already expensive care!

Two ways to minimize the cost of a nursing home stay are to use a Roth IRA (if it is large enough) or own anLTC insurance policy. With a long-term care policy,the costs are paid by the insurance company, and you receive those benefits tax free!

Thatleaves the investment accounts untouched and able to continue growing and supporting life’s other expenses.

Long Term Care Insurance Premiums

When we are comparing the premiums for a LTCi policy with self-funding, we must compare the after-tax cost of self-funding care to make a valid comparison.

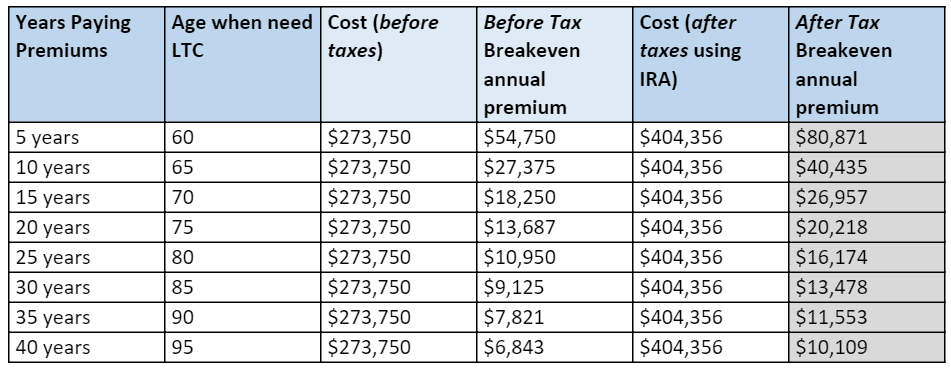

The total cost for two years of nursing home care in San Diego county in this example is $273,750. How much would premiums need to be to come out ahead?

If this couplebuys a policy at age 55 and the gentleman needs his two years of care after X years, let’s look at a simplified example to see what premium amount they could pay and still come out ahead on an after–tax comparison basis. (This chart is simplified because premiums and cost of care are not increasing with inflation.)

If their premium is lower than the column on right, they come out ahead by purchasing long term care insurance in this example.

The caveat being that premiums will increase as time goes by. But,so will the cost of care. Investment account values may not increase enough to keep up.

By buying LTCi, they are passing the risk of affording the future costs to the insurance company rather than trying to keep up with the costs throughtheir own investment accounts.

If costs rise by 5% annually for LTC, as they have been doing, then their investment account must also increase that fast. For an investment account to average a 5% or larger return, it requires a large allocation to stocks. Perhaps more than most retirees are comfortable with.

Conclusion

Owning long-term care insurance can effectively protect the lifestyle of the remaining spouse.

There are more variables to look at than are discussed in this post, but the idea is to show you thatincorporating long-term care insurance in your financial plan may be worth a close examination.

Christine Benz is very well known in retirement planning circles due to her work at Morningstar where she does retirement research on portfolio planning topics. She gave a talk to the American Association of Individual Investors (AAII) San Diego group in November 2019.

Since I have read many of Christine Benz’s articles on the Morningstar.com website, and the topic of her talk was obviously relevant to my work, I thought it would be good to go and see her in person.

The AAII group meets in Solana Beach once a month and when they have interesting speakers, I try to go. The meeting is open to anyone and is only $8.

Retirement Date Risk

The first risk Christine Benz talked about was retirement date risk. Often someone must retire at a point in time other than when they plan to retire or expect to retire. This early or late retirement date could be a result of health issues, family issues, job layoffs, or other reasons.

This is retirement date risk.

Forced retirement is a problem because it decreases the time for saving. If you have a financial plan, you know you need to save X amount per year for so many more years and your safe retirement spending will be Y. If your ability to save is cut short, then your retirement spending will have to be cut as well.

For many people who are laid off late in their career, finding a new job that pays as well as the one they left is very difficult to do.

Another major cause of retirement date risk is health issues. Either your own, or a spouse’s health issues, or someone else in your family like your parents. This can force you to reduce your work load and therefore your savings rate.

This graph from Ms. Benz’ presentation shows that more often people retired earlier than they were expecting, rather than have to work longer than they were expecting. 25% of pre-retirees were expecting to retire at 64 or younger (blue bars), but 70% of retirees actually retired before 65 (green bars).

Early retirement is very common and therefore you need to be ready in case that happens.

The way to overcome retirement date risk is to save more than you think you should. Rather than planning for a perfect scenario to play out at age 65, plan for having enough money by 60 or 62. Try and save more money so that a forced retirement date does not require you to live the remainder of your life with a reduced spending ability.

Sequence of Return Risk

When you first retire, you are at your most susceptible point in terms of stock market returns.

If the stock market goes down immediately after you retire, your likelihood of retirement success also goes down.

The worst point in time to retire since World War II was 1969. The safe withdrawal rate for a new retiree in 1969 was 4% per year adjusted for inflation. As a comparison, those who retired in 1981 were able to withdraw 8.5% per year adjusted for inflation without running out of money after 30 years. That is a huge difference! That’s the sequence of returns risk.

How does one overcome the sequence of returns risk? By not selling stocks to cover living expenses.

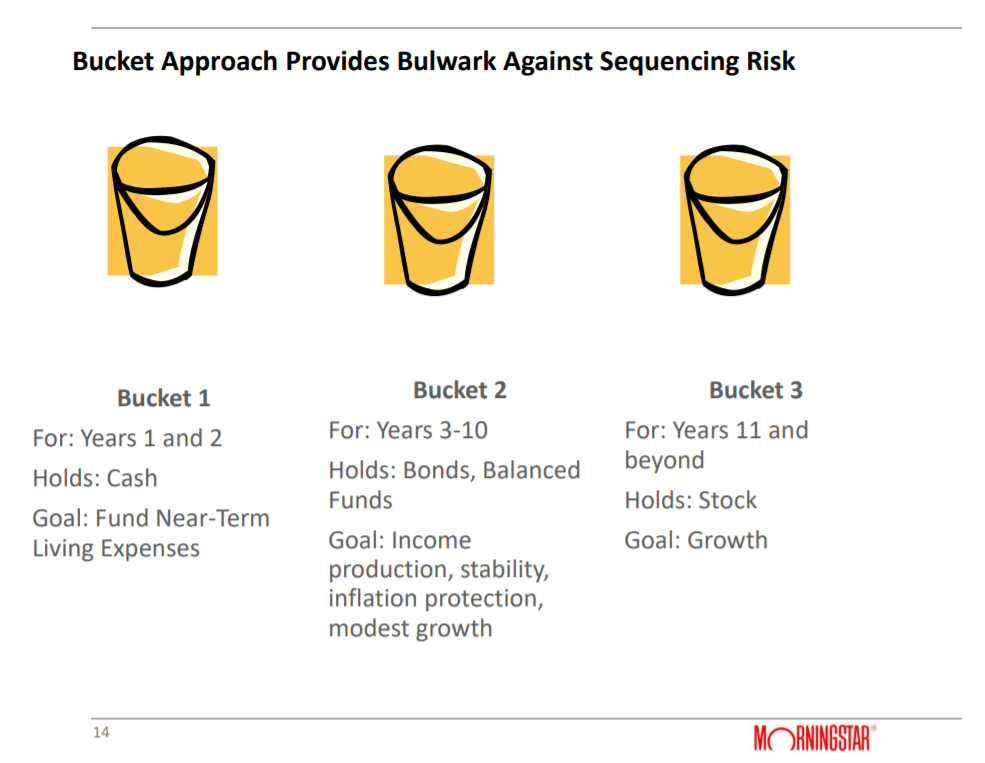

Christine Benz recommends the bucket portfolio.

With the bucket portfolio approach you keep a few years of living expenses in cash, the next few years of living expenses in bonds, and the remainder in stocks. The idea is that as you spend the cash, each year you replenish your cash from your bonds and then you replenish your bonds from your stocks when the market stock market is in an up year.

Another take on this idea of retirement withdrawal strategy (that I’ve written about before), is by Michael McClung and described in his book Living Off Your Money. Essentially his idea is that you sell bonds when you need money and then only replenish those bonds when the market has gone up 20% inflation adjusted.

The benefit of both these strategies is the fact that you’re not forced to sell stocks when they are at their lowest point.

Low-Yield Risk

Another risk for retirees who would like to live off the interest from safe investments is the low yield world we now live in.

I went to a fixed income conference in San Diego in November a couple weeks ago and the keynote speaker, James Bianco, believes we will be in a low rate environment for many years to come.

What this means for retirees is you can’t just buy CD’s and live off the interest generated. Retirees are forced to own a higher percentage of stocks than they were in previous decades.

The way to overcome this low yield risk is to invest not for income, but to invest for total return.

This means that you should consider not just the interest an investment earns, but also the change in underlying value. Bonds not only pay interest, but they go up and down in value each day the bond market is open.

It is unlikely a retiree will be able to live off the mid 2% interest an aggregate bond fund generates these days (unless they have a lot saved or need little). To withdraw 4% from their accounts, retirees should consider the 2% interest payments along with both the change in value of the bonds and the change in value of the stocks they own. The portfolio should be thought of as a whole, as total return.

The incorrect way to overcome this low yield risk according to Ms. Benz is to invest in risky bonds. Retirees should not reach for yield by putting their life savings in high yield bonds or emerging market bonds. The risk it’s just too high and the yield that you get is still minimal. It is better to use a comprehensive bucket portfolio type approach to create enough money to live off.

Inflation Risk

With 3% inflation everything costs double after 24 years. That’s inflation risk.

By the time you are 20 years into your retirement, things are going to cost a lot more than they do now. We have all seen prices go up and know it will continue to happen.

Although inflation has been less than 2% in recent years, the items that retirees spend money on (mainly healthcare and travel) are inflating at a higher rate than general inflation.

Ms. Benz says the way to overcome inflation risk is to make sure you own enough stocks. Over time, the stock market has increased more than inflation and should continue to do so.

I think you should also own some real estate investment trusts (REITs), and possibly Treasury inflation protected securities (TIPS) as part of your bond portfolio.

Another way to overcome inflation risk is to delay Social Security for as long as possible. Each year you wait to claim Social Security, your check increases by 8%. Since Social Security has a cost of living adjustment, waiting to claim will not only bring a bigger Social Security check, it will also bring larger increases each year.

Another strategy to overcome inflation risk is to purchase an inflation protected annuity large enough to cover your basic, necessary expenses. This guarantees you have at least your living expenses covered, no matter what the stock and bond markets do in a particular year.

Healthcare / LTC Risk

As we get older, we generally need more healthcare and unfortunately for older people, health care costs have been inflating faster than other living expenses. That means healthcare becomes an increasingly large portion of a retiree’s expenses as they age.

The way to overcome this is to stay healthy.

Financially the only way to overcome this is to budget for increasing healthcare expenses. There are no easy solutions to this. One thing working in favor of affording these higher medical expenses is that overall spending in retirement tends to stay constant because as we age, more is spent on healthcare, but less is spent on travel and activities.

Even if you have a Medicare Advantage plan with no monthly fee, the price of Part A and B, your deductibles, prescription costs, and out-of-pocket expenses are likely to increase each year. For 2020, the increase in Part B is 7%!

Another health care cost risk, that often isn’t thought about, is the fact that if you retire early, you have to go to the exchanges to buy healthcare insurance for the years between your retirement date and age 65 when you begin Medicare.

These rates are often well over $1000 a month for a couple. An additional $12,000 a year is a very large expense for a retiree. This additional expense is not just for those who have the means to retire early, those who are forced to retire early would have to go to the exchanges for health care as well.

Another risk is long term care risk. Long term care is not covered by Medicare or health insurance, and it refers to things you may need help with if your health has deteriorated or you’re old. Activities of daily living like bathing, getting out of bed, getting dressed, feeding yourself, etc.

In 2019, the average cost of one year’s worth of in-home health aide in San Diego County is $64,000. That is a significant expense and may be needed for many years. Nursing home care would cost even more.

The most common plan for long term care costs is to use home equity. If you don’t own your home, or don’t have a lot of equity built up, long term care needs could use up the vast majority portion of your portfolio.

There are long term care insurance plans available which are usually very expensive. To alleviate the worry that you’re going to buy long term care insurance and never need it, there are now combination/ hybrid long term care insurance plans with life insurance. This means either you will get the use of the long term care insurance, or your heirs will get a life insurance benefit if you pass without using all the long term care insurance benefit.

Longevity Risk

What if you have a nice long life and live to age 100 or more? That may seem unlikely or very far in the future, but if it could happen. For a couple, both age 65, there is a 31% chance (almost one-third) that at least one person will live to age 95. Future improvements in personalized medicine may increase these odds.

Financially speaking, living that long could take a toll. To overcome this risk, you need to put together a plan that uses all the available techniques.

Invest enough of your assets in stocks, use a total return approach, have a tax-efficient withdrawal strategy, maximize your Social Security and pension benefits, live within your means, and be flexible with your spending, consider annuities, and others.

Those are the 6 retirement risks and how to overcome them according to Christine Benz of Morningstar. If you have any questions about these risks, how they apply to your situation, or want some financial planning advice, please contact me.

If you receive a pension, what stock allocation percentage should you use in your investment accounts?

Every retiree or soon to be retiree needs to determine how much of their investments to place in stocks.

The standard answer for retirees is that a 50% – 60% stock allocation maximizes portfolio longevity. If a retiree receives a pension or other guaranteed income like an annuity, then 50% – 60% may not be the best answer.

Guaranteed or annuitized income increases the safety of your retirement. Someone without guaranteed income must fund 100% of their retirement spending needs solely from investments. To remain solvent throughout their lifetime, they must err on the conservative side (own a higher percentage of bonds and cash) to provide a buffer during years the market is down.

On the other hand, if you have enough guaranteed income to cover at least your basic lifestyle needs, then you can let your stock investments fluctuate without it impacting your retirement safety.

Current Research

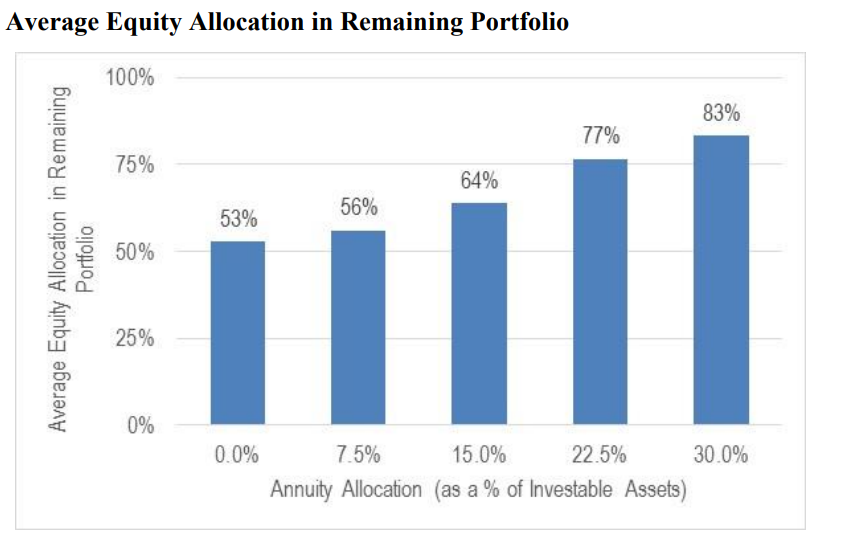

Let’s look at what the current research has to say about the optimal stock allocation when one has various portions of their income guaranteed. The research behind the calculations comes from an article published in the Journal of Financial Planning, November 2018 issue. The article was titled “Annuitized Income and Optimal Equity Allocation” by David M. Blanchett, Ph.D., CFA, CFP® and Michael Finke, Ph.D. CFP®.

The results are based on a couple both age 65 who will live slightly longer than the Social Security mortality rates predict, and their guaranteed income increases each year with inflation. The following chart shows the results combined into graph form to show the average allocation to stocks when compared to percentage in annuitized income.

The trend is clear. The more guaranteed income a retiree has, the higher the optimal allocation to stocks. This is due to the safety the guaranteed income provides.

Pensioners and annuitants can handle more market volatility than other retirees.

Example

Let’s look at an example for a retired couple who have $600k of investments and would like an income of $95,000 per year, before taxes. The gentleman receives a $77,000 pension annually. To make up the difference, they must withdraw $18,000 per year from their investment accounts. That is a 3% withdrawal rate($18k/$600k).

First, we need to calculate the value of his guaranteed income. These calculations are explained in this post: What is a Pension Worth?. His pension is worth $1,670,900. Therefore, the percentage of this couple’s wealth that is in annuitized income is therefore 74%:

$1,670,900/$2,270,900 = 74%

(The $2.27 million figure comes from adding his pension value to their investment value: 1,670,900 + 600,000 = 2,270,900)

Using the chart provided in the research article, they should be invested at an allocation of 70% stocks to maximize their lifetime income and legacy to their children or charities.

If you have questions about your own investment allocation or how your pension, investments, Social Security and other aspects of your finances will come together in retirement, please click here to schedule a free meeting.

In this post I am going to show you a method for calculating your pension value.

You can use these calculations to determine how much you would need in a retirement account (401(k)/403(b)/IRA) to safely withdraw an amount equal to your pension income.

The research behind the calculations comes from an article published in the Journal of Financial Planning, November 2018 issue. The article was titled “Annuitized Income and Optimal Equity Allocation”.

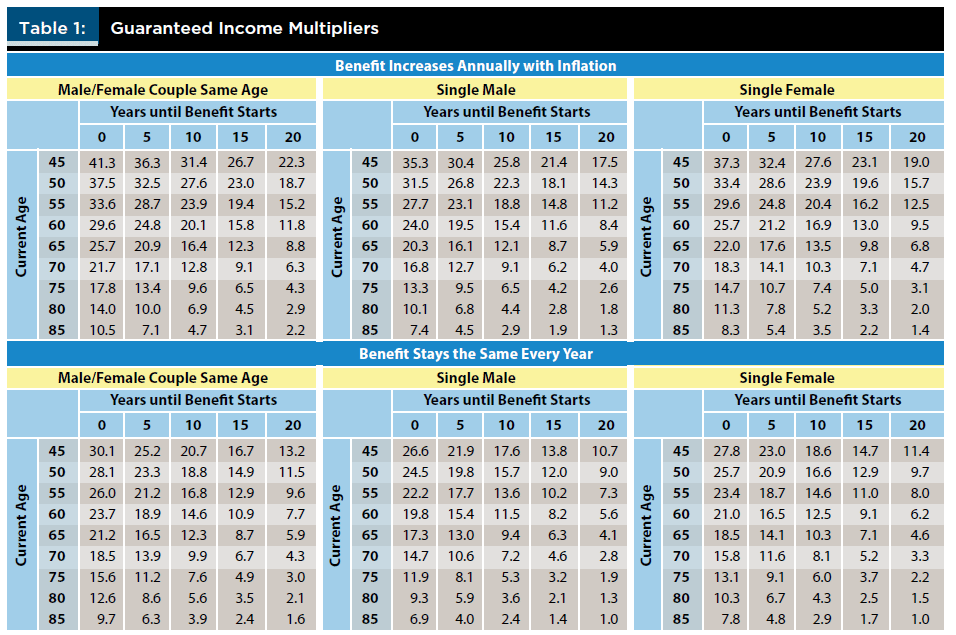

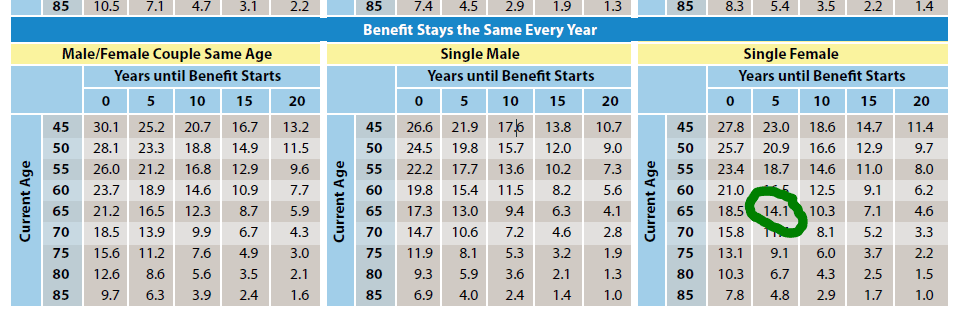

Here is the Income Multiplier chart from the research article:

In our first example, a pensioner receives $77,000/ year and that pension income increases with inflation. This pensioner is 70 years old, and his wife is of similar age.

Since his pension has a cost-of-living increase, we are using the top row of three results in the chart. His pension has already started so we will use column “0”. We find his multiplier is 21.7.

To calculate his pension’s value, we take his annual pension income and multiply it by 21.7.

$77,000 x 21.7 = $1,670,900 !!

So, for this couple to confidently withdraw an inflation adjusted $77,000 annually for the rest of their lives, they would need to have an additional investment account with $1.67 million in it!

Let’s look at two other examples and calculate how valuable their pensions are.

Next, we look at a firefighter captain who is retiring at age 55. His pension is $85,000. He is unmarried and so we will use the single male chart in the middle of the top row.

From the chart, we find his multiplier is 27.7.

Calculating the value of his pension means $85,000 times 27.7 for a total of $2,354,500 !!

This gentleman would have needed to have a high paying job to have accumulated $2.3 million by the age of 55! Instead, he risked his life and survived with a guaranteed income stream.

Not all pensions are large. Some will cover only a small portion of your expenses in retirement. For example, a lady had worked in the grocery industry when she was younger. She was entitled to a pension of $9,000 per year with no inflation increase, ends upon her death, and starts five years from now. She is currently 65 years old.

How much would an equivalent savings amount be?

From the chart above, we find her multiplier. It is 14.1.

$9,000 x 14.1 = $126,900!

From these examples, you can see that a pension is an extremely valuable asset.

It would take manyyears of saving and successful investing to accumulate an equivalent amount.

What does a financial plan look like? (Updated 2022)

In this blog post I am going to show you highlights of a sample financial plan for a couple approaching retirement.

Each section of a financial plan from Andrew Marshall Financial, LLC includes a written discussion of the topic, my recommendation for your best course of action, the reasoning behind that recommendation, and data, diagrams, or other evidence to support the recommendation.

I am not going to show an entire financial plan here. In a financial plan, the discussion of each section can be extensive. This sample retirement plan was 13 pages when printed.

This post should still give you a good idea for what to expect when you hire us to create your financial plan.

Not Mike or Susan

The sample financial plan we are going to look at here is for two clients named Mike and Susan.

Mike and Susan are baby boomers with two grown children who no longer require their support. Susan has just retired from Kaiser Permanente and Mike is still working.

Mike and Susan have been managing their finances on their own,but with retirement approaching, they want a professional opinion to confirm they can retire as expected and to make sure they are not missing something they are unaware of.

Let’s go through some highlights of their financial plan.

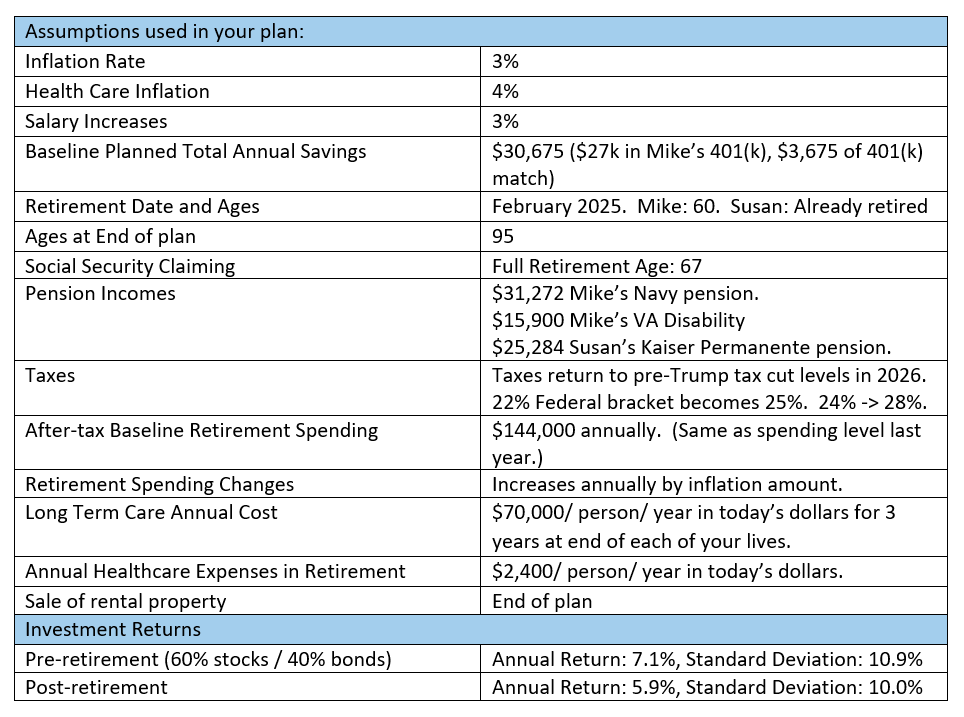

After looking at where they currently stand, we review some assumptions used in the financial plan.

Assumptions are an integral part of any financial plan. We must assume certain inflation rates, investment returns, savings amounts, life expectancy and others to be able to do the necessary calculations.

Those assumptions are laid out near the beginning of the plan, so they are known to all.

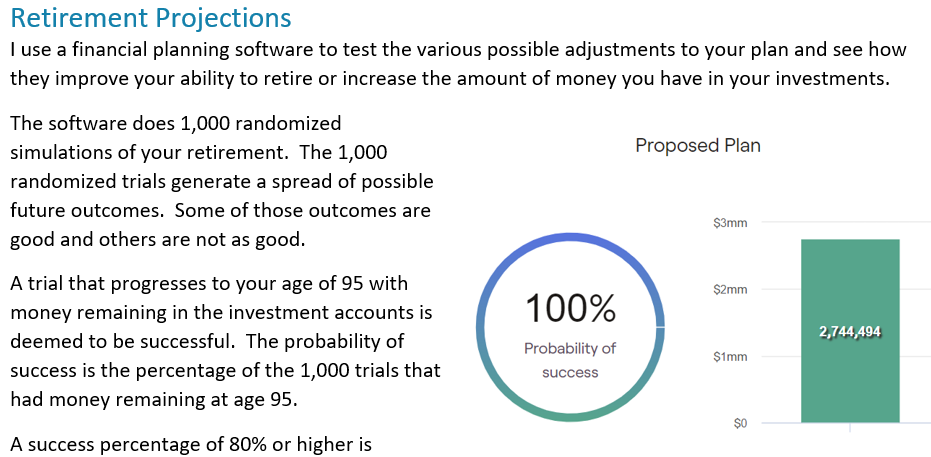

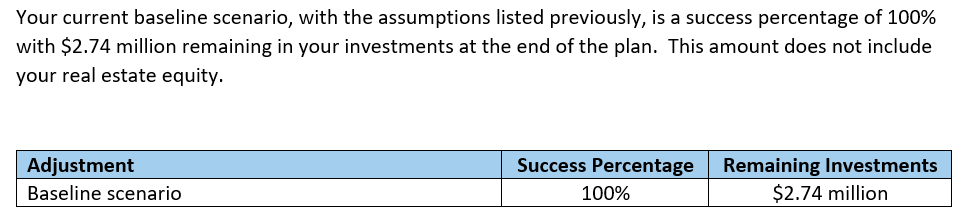

Our financial planning software does Monte Carlo analysis to project the probability of success in the future. In financial planning terms, this is the chance that you will still have money remaining in your investment accounts at age 95, with the assumptions above.

Using the assumptions and the software, we come up with a baseline scenario. For Mike and Susan the outcomes are excellent.

From here we can test various options and changes to what they are currently doing to maximize their retirement outcomes in terms of success percentage and ending assets.

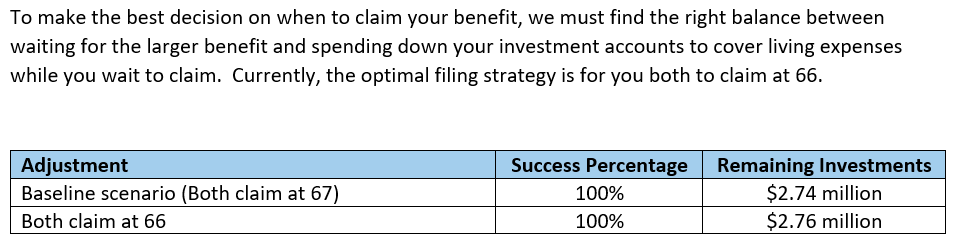

The first topic is a discussion of Social Security claiming strategies and how those strategies impact the retirement plan.

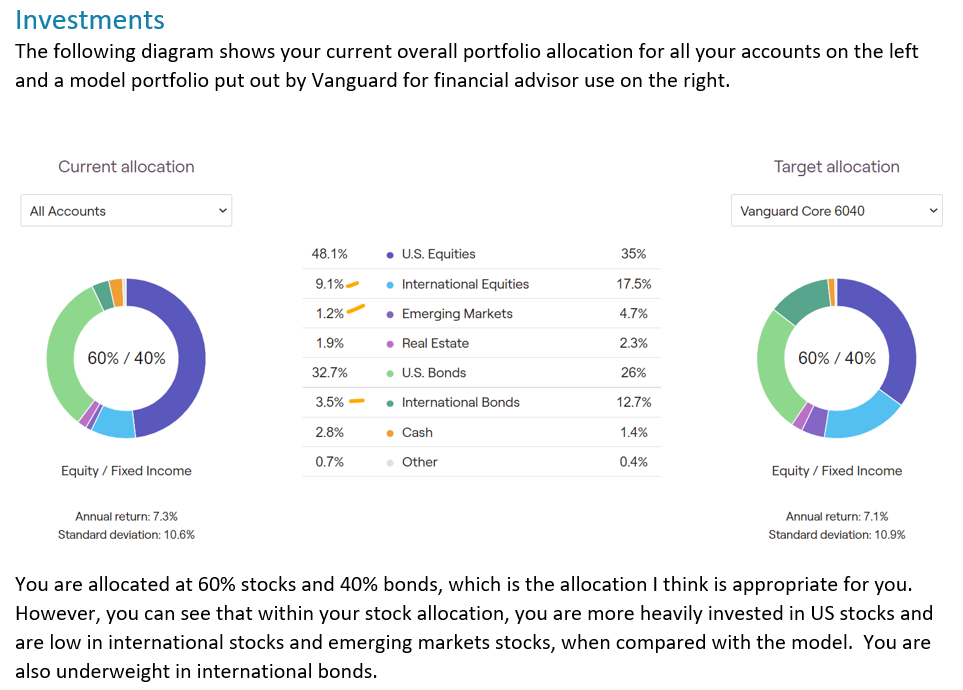

Every plan has a section covering investment review and analysis.

If you have multiple investment accounts like IRA’s, Roth IRA’s, 401(k)‘s, taxable accounts,and others, then I will review all of your accounts and create a cohesive plan that optimizes each account.A discussion of each account and the recommended adjustments is included. If selling and buying of funds are recommended, they are listed out by fund, amount, and account, to make it as easy as possible to implement the adjustments.

This sample plan includes a discussion of Susan’s pension options. This was a long, multiple page section explaining the risks and benefits of each option.

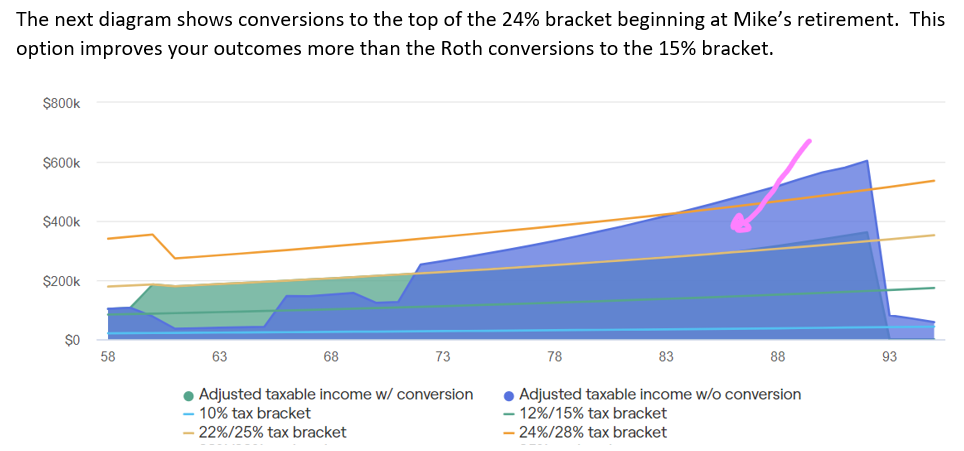

There is also a discussion about Roth conversion strategies and a chart showing how conversions would improve their retirement outcomes.

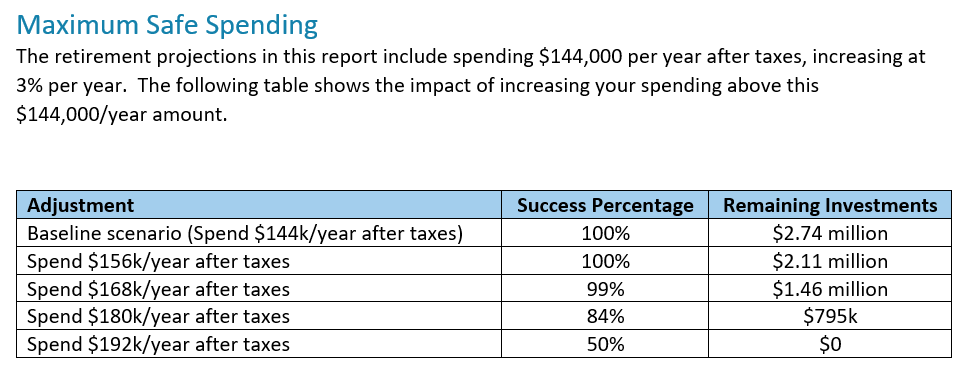

A popular topic is what is the maximum safe spending possible in retirement. The following graphic shows the impact of Mike and Susan increasing their spending in retirement.

Finally, they were interested in long term care insurance. A discussion of the risks, a quote for long term care insurance, and a review of whether they can self-fund are included.

The culmination of all the analysis and discussions in this example financial plan is the creation of a written retirement plan that Mike and Susan can use to implement the changes and refer back to as needed.

The topics covered in your financial plan will likely be different from this sample retirement plan. Your topics are decided upon when we first meet.

Additional topics you may be interested in include:

what account is best to save money in,

how should you withdraw from your accounts once you retire,

a review of your tax return,

stress testing the success percentage,

including a reverse mortgage at retirement,

should you pay off your mortgage early,

do you need to keep your life insurance policies,

and many others.

As for future updates to your plan, I leave it up to you. I would recommend Mike and Susan update their financial plan each year to make sure they stay on track to retire. For an update, we will repeat the process of deciding what work you need done, generating a quote, signing a contract extension, and then doing the work.

If you would like to talk about creating your financial plan, call (760) 651-6315 orschedule your first meeting.

A Roth IRA account is a great way to create a million dollar retirement.

Types of IRAs –

There are two main types of IRAs, atraditional IRA and a Roth IRA. The taxes on these two accounts work differently.

Contributions to a traditional IRA are tax deductible now, and taxes are paid when you take withdrawals.

Contrarily, contributions to Roth IRAs are not deductible now. You pay tax on the money before you contribute to the Roth. In exchange for paying your taxes this year, the government lets you take money out tax free when you are old enough. (A long list of rules and restrictions exist for both IRAs. The above is a simplified description.)

Choosing an IRA type –

Why choose a Roth IRA over a traditional IRA? It depends on your situation, but paying your taxes now may be beneficial. Most people imagine they will be making more money in the future.

How unsatisfactory would your retirement be if you have to live on the same amount of money you were making in your thirties? Instead, most of us plan on increasing our incomes and wealth throughout our careers.

When you will have more wealth in the future, you should choose a Roth IRA over the traditional IRA. (If your income makes you ineligible for one, consider a backdoor Roth IRA). Under this situation, you will be paying taxes at today’s income rate and then withdrawing it when you are in a higher tax bracket. Tax-free Roth IRA withdrawals will be advantageous.

IRA income and contribution limits for 2019 –

The income cut off limits for 2019 are $137,000 for single filers and $203,000 for MFJ. Each year you have earned income less than the cutoff, but greater than $6,000, you can contribute $6,000. If you are 50 or over, you can contribute an additional $1,000.

Contributing $6,000 may not sound like it could produce a large account, but adding $6,000 to the account each year adds up over time.

Account size calculations –

Let’s look at some calculations to see just how much we can save by retirement. And remember, this amount will be tax free!

$6,000/ yr

Age 30 to 67

Investment return = 0%

Value = $220,000

Without earning any interest or investment return, we would have saved $220,000 by contributing at age 30 until full retirement age of 67. Being able to save $6,000 per year, or $500 per month should be possible from age 30 and onward. If not, you need to do some budgeting work.

Now let’s change our return to a fairly conservative 5%.

$6,000/ yr

Age 30 to 67

Investment return = 5%

Value = $640,257

Wow. Over half-a-million, tax-free dollars could be yours for saving $500 per month and investing conservatively. By conservatively I mean 30% US stocks and 70% intermediate Treasuries. According to Portfoliovisualizer.com, that allocation would have been enough to produce a 5% inflation adjusted return.

Next let’s change the investment return. Since this is a long-term account, the proper investment strategy would be to invest aggressively in a high percentage of stocks. With a more aggressive 8% return, the following account values are possible.

$6,000/ yr

Age 30 to 67

Investment return = 8%

Value = $1,315,895

Check out that result! (In reality this number could actually be higher than $1.3 million because the contribution limit will not remain at $6,000 for the next 37 years. It has increased at 4% per year since 2002 when it was $3,000.)

Calculations for starting late –

What if you are not thirty anymore, but 40 years old instead? Let’s take a look at how much you could save.

$6,000/ yr

Age 40 to 67

Investment return = 8%

Value = $566,032

Or alternatively, you are now 50 years old and trying to make a big push to accumulate a nice nest egg before retiring at age 67. That gives you 17 years of contributions and a contribution limit of $7,000 because you are now eligible for the catchup contribution.

$7,000/ yr

Age 50 to 67

Investment return = 8%

Value = $255,151

That’s over a quarter of a million dollars tax-free for your retirement. If you didn’t touch that money for an additional ten years, it could be worth $550,851.

That’s a good sum of tax-free money that could be used to pay for health care, long-term care, nursing or home health care or other expenses in old age.

Conclusion –

These calculations show us that it is possible to accumulate a tax-free 1 million dollars for retirement with annual savings and investing in a Roth IRA account.

Remember, these values are only in your Roth IRA. You will also have your 401(k) and other investment accounts. It is definitely worth your effort to open a Roth IRA account, contribute the maximum each year, and invest in it aggressively.

If you would like to talk to me about this or other investing ideas, call (760) 651-6315.

Should you open a SEPIRA or SimpleIRA if you are a one-person business?

This review is for a one-person business whose owner is age 50 or over. It is NOT from the point of view of a small business with a few employees. We will look at which is the better choice under two conditions; when your self-employment income is your primary income and when it’s a secondary income. (The numbers discussed are 2019 limits.)

SEP IRA stands for simplified employee pension individual retirement account. Both the SEP IRA and SIMPLE IRA are defined contribution retirement plans. Both enable you to defer taxes until after retirement.

When investigating or thinking about these types of retirement plans, you need to remember that as a self-employed person you are both the employer and the employee.

The SEP IRA contributions come from your employer side. The SIMPLE IRA contributions are actually employee salary reduction contributions from your employee side.

In 2019, the maximum retirement contributions for the two plans if you are 50 or over are:

SEP-IRA: The lesser of 20% of compensation or $56,000.

SIMPLE: $16,000 for employee contributions plus a SIMPLE IRA employer matching contribution of 3% of compensation up to 3% of $280,000, or $8,400 maximum. Maximum total of $24,400.

Before we go into the details of each scenario, there are two possibilities where your decision is easier.

If there is a chance you will hire employees in the next couple of years, choose a SIMPLE IRA plan.

If you make less than $100,750 per year and you don’t see yourself making more than that from your self-employment income, then choose a SIMPLE IRA plan. (I used this retirement contribution calculator to arrive at the break even number of $100,750. https://www.calcxml.com/calculators/qua12 )

Which should you choose if you have another job?

In this scenario, you have another job and your self-employed income is a secondary income source. Perhaps you drive Uber or have a side business. At your main job you have a 401(k) plan and make the maximum 401(k) contribution of $25,000 every year. You want to defer taxes on as much of your secondary income as possible, to boost your retirement savings.

Remember the picture of two pockets and the fact that as a self-employed person you are both employer and employee? SEP IRA contributions come from the employer side while SIMPLE IRA contributions come from your employee side.

The maximum allowable employee salary reduction contributions are $25,000 total annually, in all such retirement plans. Your 401(k) contribution at your main job comes from this employee side and therefore, you cannot contribute to a SIMPLE IRA if you are already contributing $25,000 to a 401(k).

Since SEP IRA contributions come from the employer side, you could contribute the $25,000 to your 401(k) and also 20% of your self-employed income to your SEP IRA plan.

So, if your self-employed income is a secondary income, you should open a SEP IRA.

What if your self-employed income is your main income?

Since either the SEP IRA or SIMPLE IRA will be your main retirement plan, the decision will come down to which plan has a higher contribution limit.

If you make less than the break even number ($100,750) discussed above, say $50,000 for example, then your maximum contributions to a SEP IRA would be $10,000 and to a SIMPLE IRA would be $17,500. You should choose the SIMPLE IRA because you would be able to save an additional $7,500 tax deferred.

If you make more than the break even point, such as $120,000, then the maximum contribution to a SEP IRA is $24,000 and to a SIMPLE IRA is $19,600. You should choose the SEP IRA.

Is there a significant difference in annual maintenance or IRS reporting requirements?

No. Neither plan requires any reporting to the IRS. The custodian where your accounts are held will take care of all the required paperwork when you open either IRA account.

Impact on Traditional and Roth IRA contributions.

With both the SEP IRA and SIMPLE IRAs, you are still eligible to own and contribute to a Traditional IRA or a Roth IRA. That means you still have the opportunity to contribute another $7,000 for retirement, regardless of which plan you choose.

The 2018 tax write-off decision factor.

The month of the year when you are making this decision may sway you. You can open a new SEP IRA anytime up until you pay your taxes in the following year. So, as I am writing this in February of 2019, you still have until April 17, 2019 to open a new SEP IRA, make contributions for 2018, and therefore get the tax deduction on your 2018 tax return.

The deadline for opening a SIMPLE IRA for 2018 passed on October 1, 2018. You can no longer open a SIMPLE IRA and use it to reduce your 2018 taxes due. If you open a SIMPLE IRA today, the contributions you make will be for 2019.

If you are making this decision or another decision about your retirement plan and would like our help, call us at (760) 651-6315 or email contactus@andrewmarshallfinancial.com.