This is a written summary of a video I posted on YouTube.

Introduction

Recently, I worked with a client couple who were considering using Schwab Intelligent Portfolios, a Robo-advisor, for managing their retirement funds. This got me wondering whether using a Robo-advisor or all-in-one self-rebalancing fund is indeed the best strategy for retirees, or if a more traditional approach of managing stocks and bonds separately would yield better results.

In this article, we’ll explore both these options in the context of a retirement withdrawal account and examine which one proves more beneficial.

Robo-Advisors vs. Traditional Portfolio Management

In this study I wanted to compare automatically rebalanced solutions. This includes robo-advisors and mutual funds or ETFs that rebalance automatically. Examples of such funds include target-date funds, Vanguard Life Cycle funds, balanced funds, income funds, Vanguard Wellington and Wellesley funds, and others.

What Are Robo-Advisors?

Robo-advisors like Schwab Intelligent Portfolios are automated platforms that manage your investment portfolio using algorithms. They automatically rebalance your portfolio to maintain a set asset allocation, which can relieve investors from the day-to-day management of their investments.

Traditional Portfolio Management

In contrast, traditional portfolio management involves manually balancing your investments, where you maintain separate holdings for stocks and bonds. This allows the investor to decide which assets to sell based on market conditions, giving them more control over their outcomes.

The Case Study

To determine which strategy works better for retirees, I conducted a case study using two different 5-year periods.

- 1999 to 2003 – this included the dot-com bubble.

- 2019 to 2023 – this timeframe included the COVID-19 crash and subsequent recovery, followed by the 2022 bear market.

Methodology

– The portfolio starts with $1 million.

– $50,000 is withdrawn each January.

Here are the selling rules which made keeping stocks and bonds separate the better technique.

– Withdraw from stocks if the previous year’s returns are positive.

– Withdraw from bonds if the previous year’s returns are negative.

I used Portfolio Visualizer to determine the portfolio returns. Its new interface is somewhat confusing, so I used the Legacy User Interface to conduct my analysis.

For the traditional management account, I used:

– Vanguard Total Stock Market Fund (VTSMX)

– Vanguard Total Bond Market Fund (VBMFX)

For the Robo-advisor / All-in-one setup, I assumed a fixed 60/40 stock-to-bond ratio of the two funds. I had the portfolio set to rebalance monthly to approximate the auto-rebalancing of the robo or funds.

Analysis and Results

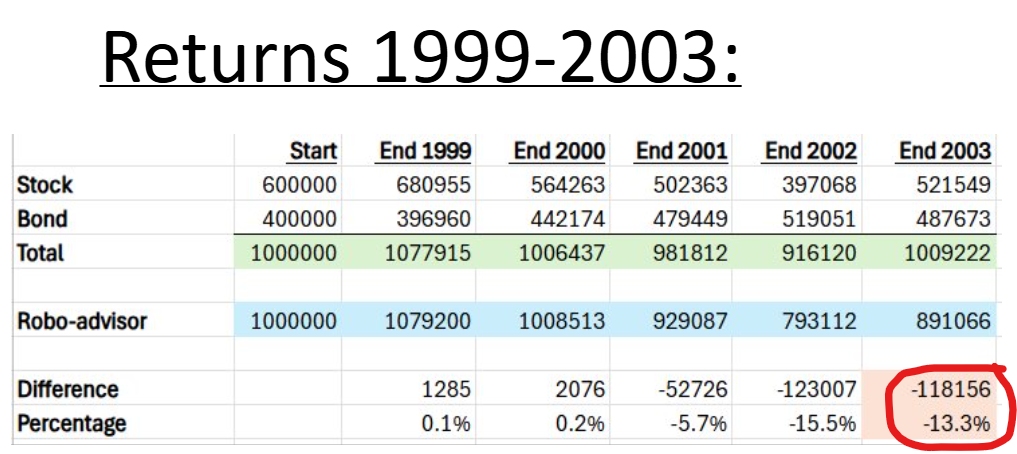

1999 to 2003 (Dot-Com Bubble)

– Withdrawals were made from stocks in 1999 and 2000.

– Withdrawals from bonds in all other years.

Starting Portfolio Value was $1,000,000.

Ending Portfolio Values:

– Self-managed portfolio: $1,009,222

– Robo-advisor portfolio: $891,066

Managing the portfolio manually resulted in 13% higher ending portfolio values! That is a significant difference.

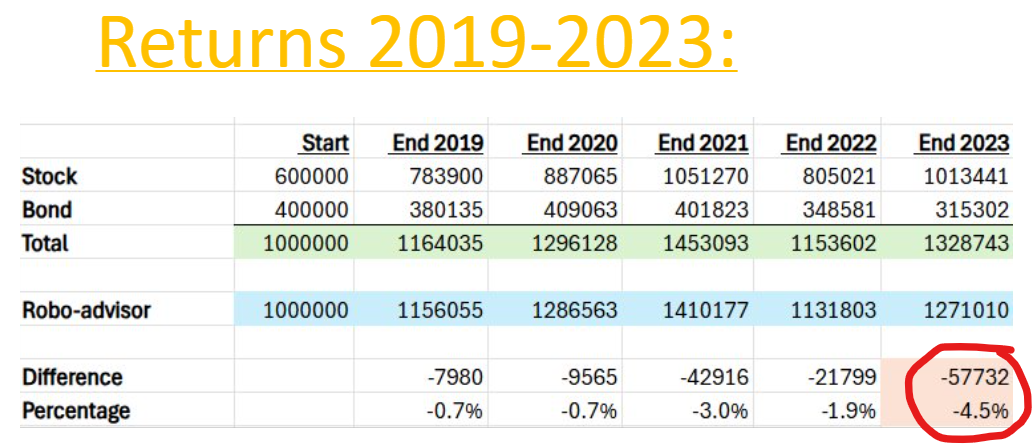

2019 to 2023 (COVID-19 Crash and Recovery)

– Withdrawals were made from bonds in 2019 and 2023.

– Withdrawals from stocks in all other years.

Starting Portfolio Value was $1,000,000.

Ending Portfolio Values:

– Self-managed portfolio: $1,328,000

– Robo-advisor portfolio: $1,271,000

While the difference here is less pronounced compared to the first period (only a 4.5% difference), the self-managed portfolio still outperformed the Robo-advisor / All-in-one Fund. This outcome suggests that during periods of strong stock market performance, self-managing your investments can contribute to better financial outcomes, but the real advantage occurs when the market is down.

Implications for Retirees

Self-managing your investments can really pay off during times when the stock market is down. By selling bonds to generate cash in down stock market years, the stock portion can recover faster, which leads to larger portfolio balances.

I understand self-managing your investments takes some time and effort, but one option that would limit the time needed, is to self-manage your first priority withdrawal account and use an all-in-one fund or robo-advisor to manage your other accounts.

To set up a free-first meeting with Andrew please CLICK HERE.