Do you want objective financial advice? Are you comfortable managing your own investments at Fidelity, Schwab, Vanguard, or others? Then you should consider hiring an hourly financial advisor when you need advice.

Finding a financial advisor or a financial planner who will charge solely by the hour for their time spent is not an easy search.

There are many advisors who will tell you they will charge by the hour when you first meet them, but really, they prefer to charge based on the size of your investment accounts. This is called AUM fees or assets under management.

I have heard from clients that they spent a lot of time searching for an hourly advisor and thought they had found one, only to later find out the advisor really wanted them to sign over control of their investments.

Where do you find an hourly financial advisor? On the internet at one of the following websites.

My first suggestion for where to look to find hourly financial advice is the Garrett Planning Network. The Garrett Planning Network was founded with the intent of providing competent advice to people who do not meet the usual qualifications advisors look for. (That generally means a large investment account that can be managed for ongoing AUM fees.) I am a proud member of the Garrett Planning Network.

If you go to the Garrett website, click in the top right, and scroll down to hourly only, you can see a list of advisors nationwide who do not charge or offer AUM. Choosing one of these advisors means there is no way they will later ask you to hand over control of your accounts.

Another website directory of advisors who might charge by the hour is NAPFA. I used to be a member of NAPFA and my impression is that a very high percentage, like far above 90% percent, charge AUM fees. They are fee only, which means they will not charge you commissions, but very few charge solely by the hour.

On the NAPFA website you can narrow down your local search results using the funnel icon to select Hourly.

The same thing goes for the next directory. The Fee Only Network. The advisors on this site mostly charge AUM fees, but some do not. You will have to read through the descriptions or go to the advisor’s individual website to read about how they charge.

The 4th referral site is the XY Planning Network. On their site you can narrow things down to eliminate the AUM advisors by clicking on “Select Advisor Specialties” and then “Advice Only”.

“Advice Only” is a newer term that has become more popular in the past couple of years and includes hourly financial advisors but could also mean subscription or retainer types of fees.

A website directory for these planners is the Advice-Only Network.

This website does not yet have a good search function to narrow down or sort the list of advisors. You will have to scroll through the advisors and read about each one to find someone you like.

I think hourly financial advice is best for someone who is knowledgeable about personal finance concepts but would like to check in with a professional to make sure they are doing things correctly, have a question that is more complicated than they can find an answer to online, or want a second opinion.

All my clients have been managing their own investments and have no desire to hand over those management duties. They also realize there may be things they don’t know that are costing them money, especially in the long run. Paying an advisor an hourly fee to look things over and make recommendations on how to improve upon what they have been doing is money well spent.

To schedule a free first meeting with me, click here.

As you investigate financial advisors and the various methods financial advisors and financial planners use to charge for their services, you should become aware of the benefits of using an hourly, fee-only financial planner.

There are two big conflicts of interest in financial advice. The first is assets under management fees or A.U.M. fees for short. The conflict of interest in this type of fee comes from the fact the advisor earns more money from you when the account they manage is bigger. At first this may sound like a great motivation for the advisor to invest your money well, but there are times when it can be detrimental to your financial well-being, in addition to being very expensive when you actually calculate the fee.

A few examples include the financial advisor investing your account at too high a risk level. They do this in an effort to grow the account, but in a down market, the losses you experience could be very stressful for you.

They may discourage you from investing in rental real estate, even if it is a good investment. Also, they may not suggest funding a 529 plan with an up-front lump-sum amount taken from your investment account because it would lower their ongoing fees.

The second serious conflict of interest in financial services is selling insurance and insurance products like annuities for commissions. Obviously, it is difficult to trust someone who benefits financially from the sale of a product they are recommending.

At Andrew Marshall Financial, LLC we are hourly and fee-only financial planners. We do not offer AUM services and we do not sell insurance products.

By doing business this way, we avoid the two main conflicts of interest I just described. I invite you to schedule a free, first meeting to see if our services would be a good fit with your current needs.

Federal employees, State employees, teachers, union workers, and others who have most of their net worth in their pension, their work retirement account (TSP, 403(b), 457, etc.), and their home equity are a perfect fit for the consultant financial planning service offered by Andrew Marshall Financial, LLC.

Conflict free

Fee only consultant style advice, rather than assets under management (AUM) fees, aligns us with pension employees. By not requiring you move your investments, a major conflict of interest is removed and therefore, we are free to give you the most open advice possible.

Decisions such as paying off your mortgage early or leaving your investments in the TSP/ 403(b)/ 457 may be the best for you. An advisor getting paid based on your account size has a motivation to not recommend those moves.

When Andrew Marshall Financial, LLC gives advice, it is in your best interest, not ours. We are a fiduciary, and we take that seriously.

No ongoing fees

Another issue with assets under management financial advisors is they charge ongoing fees, even if they aren’t giving you financial advice. With our financial planning, you pay only for what you need, when you need it.

As you approach retirement, adjusting your course once per year is usually a good idea. Once you start your pension, you may not need ongoing advice. More likely, you will settle into your retirement lifestyle and new routine. You may only need or want financial advice every two or three years. With Andrew Marshall Financial, LLC, you only pay for advice when you need it.

The CFP board revised its Code of Ethics and Standards of Conduct effective October 1st 2019.

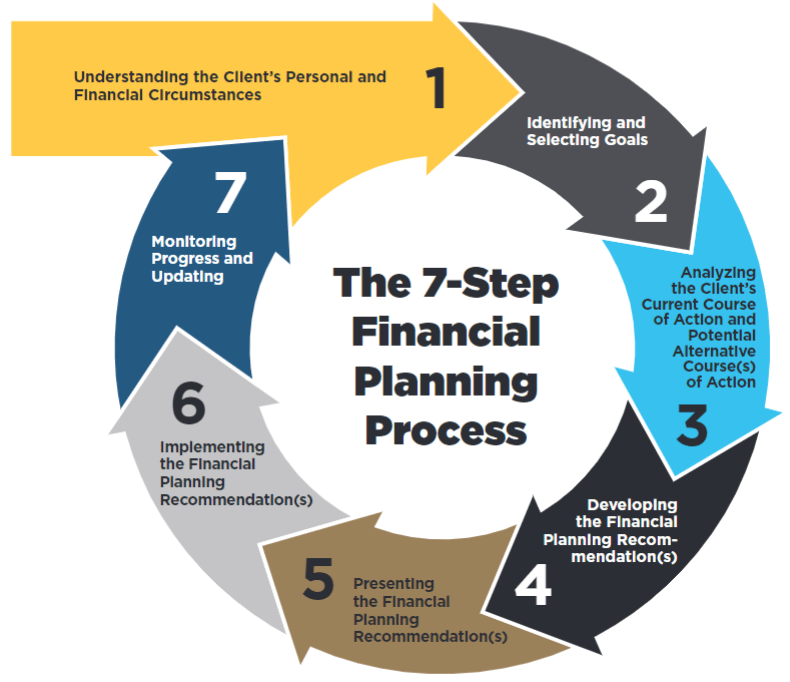

Part of this revision was an update to the CFP™ Practice Standards for the Financial Planning Process. This revised process is logical and makes a lot more sense than the previous version.

In this post, I will go through the seven steps to the revised financial planning process and show you how working with Andrew Marshall Financial, LLC (AMF) corresponds to each step.

Understanding the clients personal and financial circumstances.

The first step in the financial planning process is gaining an understanding of your personal and financial circumstances. How did you get where you are today? Who is important in your life? What assets do you have to work with in your next stage of your life journey?

To begin to understand your circumstances, I ask everyone who is considering working with AMF to complete a confidential questionnaire.

In the questionnaire I ask for some basic contact and financial information like: do you own a home, are you collecting Social Security, how many kids do you have, are you married, etc.

In the questionnaire I do not ask for any financial numbers. That way there is very little reason not to get started and fill out the questionnaire. It should take you 10 minutes or less to complete the questionnaire. A link is here.

With your questionnaire complete, the next method I use tounderstand your situation is to talk to you.

If you’re in the Carlsbad area, we can meet in my office.

If you’d rather not drive, or you’re not near the Carlsbad, California area, we can do a video conference. If you’re familiar with video conferencing at work or you have used Skype or FaceTime, you know it’s very easy to go online and meet as if we’re in the same room. The final option is a traditional phone call. Phone calls still work too.

This first meeting is free and what I want to do is hear your financial concerns, what you would like to accomplish, and determine how I can help you improve your future.

Identifying and Selecting Goals

Step 2 in the CFP Board’s financial planning process is to identify and select your goals.

You probably already know your goals before you come to see me. In our first meeting, we will talk about your goals. I may suggest some goals that you haven’t thought of but that will help your financial future.

Common goals people have are determining when they can retire, determining what their retirement spending will look like, having their investment allocation reviewed, and learning what steps they should be taking now to improve their futures.

With my help we will select and prioritize your goals. Hopefully all of your goals will be achievable, but if not, we may have to resize them or prioritize them.

After our meeting I will send you a written proposal listing out what your project will include and the price.

If you like the proposal and decide to hire me, then I will send you a contract for digital signature and collect a deposit.

After we are officially working together, my understanding of your personal and financial circumstances continues to expand.

I will collect the data needed to create your plan. Examples of the information I will collect include: your income, your spending, your risk tolerance, your account details, assets, liabilities, available resources, rental properties, taxes, employee benefits, government benefits, insurance coverages, and others.

Analyzing the client’s current course of action and potential alternative courses of action

Step 3 of the CFP™ planning process is when my work as a CERTIFIED FINANCIAL PLANNER™ professional really begins. At this stage, your input is complete for a while.

Using software, calculations, knowledge and experience, I will analyze your current course of action and create a projection for how things are likely to turn out for you should you continue as you currently are.

A baseline retirement projection is the most common example of this scenario. If you continue to save and invest as you are, you continue paying down any debts, and you retire at the age you want, what does your retirement look like? How much can you spend safely in retirement?

From this baseline situation I will test alternative courses of action to find ways to improve your outcomes. What changes to your finances will create a better future for you and your family?

My CFP™ training and experience has taught me how to analyze the different alternatives available to you and assemble them into a coordinated plan that maximizes the use of various elements and strategies.

Developing the financial planning recommendations

In step 4 of the revised CFP™ financial planning process, I will choose the best of the alternatives that I tested in the previous step to make my recommendations.

The term “best strategy” could mean many things including highest probability of not running out of money, highest net worth remaining for your heirs, highest average spending, easiest implementation, least complication, and others, depending on your wants.

In developing my recommendations, I will coordinate what the numbers tell me with what I know about you, your personality and your desires.

Once I have finished developing my recommendations, I will write a report detailing my findings, recommendations and the reasoning behind my recommendations. Click here to see sample report.

Step 5. Presenting the financial planning recommendations.

After I have completed your financial plan, we will meet again and go over the written report. I will explain each of my recommendations and answer any questions you have.

In some situations, we will connect my laptop to the large monitor on the office wall and show you how the variables affect your outcomes. For example, does spending $500 more per month make a difference? Does working one additional year make a difference? If so, how much?

As we play with the software and observe how the different elements of your financial plan interact with each other, you will come away with a great understanding of how your behavior today affects your future lifestyle.

Implementing the Financial Planning Recommendation(s)

Step 6 of the financial planning process is to implement the recommendations that you agree with. A financial plan that isn’t put into action doesn’t do any good.

When I make a recommendation for you, it’s just that a recommendation. If you don’t want to follow through on a recommendation, that’s up to you.

Hopefully I will have explained the reasoning for why my recommendations would benefit you, and you’ve asked questions, so you fully understand the recommendations.

Since I do not sell insurance and I do not manage investments, most all of the implementation will be done by you.

I can refer you to an insurance broker who works with fee only financial planners like myself, if that is needed. Also, I will make specific recommendations about funds that are available to you in your investment accounts.

For example if you have your accounts at Vanguard, I will recommend Vanguard funds for you. You can then log in to your account and make the necessary changes.

I will have analyzed your options for your 401(k) or 403(b) accounts and have made recommendations on the funds that are available to you. You can then take these recommendations, log into your 401(k) account or talk to your HR person at work, and make the changes.

In your written financial plan, I will make it clear which steps you need to implement and include instructions as needed.

Monitoring progress and updating

Since I do not charge an assets under management fee, I do not continually monitor your accounts. When you work with Andrew Marshall Financial LLC, each project is separate and the ongoing monitoring is up to you.

One way to integrate monitoring is for you to come back each year for an annual update.

During future updates we will look at how things have changed in your life and how your savings and investments have progressed. I may develop new recommendationsor adjust the current ones.

I will leave it up to you to decide how often you want to come back for monitoring your progress and updating.

This really depends a lot on the client situation. I prefer to see clients who are approaching retirement each year because the retirement transition is so critical. For clients in the middle of their careers, perhaps they can come in every 2 or 3 years.

If something changes in your life like a new job, an illness, new baby, you buy a home, etc.There are lots of things that change in life and may necessitate a progress update for your financial plan.

I hope this blog post has shown how the process I follow aligns with the financial planning process according to the new CFP board standards of conduct.

If you are ready to get started please fill out the questionnaire (link here) and schedule your first meeting (link here).

In this post I will explain why I think the answer is yes.

Charles Schwab Inc. is a huge investment company known for offering lowcost investments. They are the original discount broker.

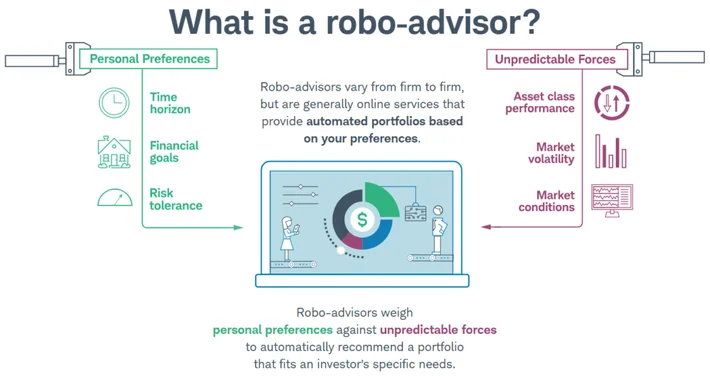

Robo advisors are automated, computer-based, systematic traders.A robo advisor is an investing tool that automates the ongoing account management steps that must be completed annually and when money is contributed or withdrawn from an account.

Robo advisors offer various investment allocations (stocks, bonds, etc.) and automatically re-balance the allocation according to certain rules.

The fact that there is a computer doing all the work means the cost is much lower than hiring a real person to oversee your investment management.

Robo investing can be especially useful for someone who is in the accumulation stage of life. One can set up a direct deposit, say $1000 a month, from their checking account. The deposit goes to their robo advisor and the computers automatically invest that additional $1000 each month in the chosen allocation.

There is no effort needed oncethe initial roboaccount and $1000 monthly deposits are set up.

That saves a lot of time for someone who’s contributing additional money, but what about a retiree who is no longer making additional contributions and who has plenty of time to manage their investments?

Just like someone in the accumulation stage, a retiree in the decumulation stage would prefer not to spend the time to log into their accounts or make a phone call to withdraw money or to re-balance their accounts every quarter, 6 months, or even once a year. That’s just a hassle, and as they get older, it might get more difficult to handle.

Here are 7 reasons why Schwab Intelligent Portfolios® are the best roboadvisor for retirees.

1. Intelligent Portfolios require a sizable allocation to cash.

Now you may not like the sound of Schwab requiring you to hold cash while they make money off your cash, but let’s think it through.

Most retirees I know are not aggressive investors and like havinga sizable amount of cash available. Maybe their cash is in a high-yield savings account or CDs, but they almost always have one to two years of living expenses in cash.

Keeping a certain percentage in cash (even 10% or more) is actually not a disadvantage. It’s something retirees would be doing anyway.

As long as the allocation to stocks is high enough, an Intelligent Portfolio investor is essentially swapping some bonds for cash (that cash earns interest at a current interest rate of 0.30% annually).

When opening an account, it is possible to adjust the stock allocation upwards to ensure enough growth in the account, even with a large cash allocation.

2.The fees = $0.

Obviously, a retirement account will last longer if one is not paying as much for investment management. One of the defining points about the Schwab intelligent portfolios is the fact there are no AUM (assets under management) fees! None!

Other roboinvesting tools such as Betterment, Wealthfront, TD Ameritrade Essential Portfolios, and others charge an annual fee of around 0.25% – 0.30% of the account value.

The reason Schwab does not charge a fee is they require a certain percentage of the account funds to be in cash. Schwab uses this cash to earn money for itself. This is not a problem for retirees – see number 1 above.

3. Schwab Intelligent Portfolios are the most diversified roboadvisor I have seen.

Maximum diversification is a benefit for retirees.

Schwab has created their own ETF’s that are not market cap weighted like typical index funds are.

The size of each stock holding within these fundamental index ETFs is based on sales, cash flow, and dividends, not price.

The Schwab intelligent portfolios service spreads one’s investments between both market cap weighted ETF’s and fundamental index weighted ETF’s. That increases diversification.

Schwab Intelligent Portfolios also spreads one’s investments across more asset classes than the other roboadvisors. Schwab includes precious metals, REITs, emerging market bonds, high-yield bonds, securitized bonds, corporate bonds, international developed bonds and others. They use up to 20 asset classes.

Maximum diversification is the best strategy for retirees. Retirees should spread their risk to help maintain their account balance should one particular type of investment experience tough times.

4. Account rebalancing is done the right way.

Accounts are re-balanced only when an asset’s allocation has drifted too far from its desired percentage.

I like the fact it is not done on a regularly timed interval but rather on a results based interval.

For example, let’s say international stocks rise and become 25% of your portfolio instead of the desired 20%. The Schwab Intelligent Portfolios algorithm recognizes this, sells some international stocks to return them to 20%, and buys bonds or other assets to rebalance their allocations. That’s the best way to rebalance an account.

“Importantly, while portfolios are monitored daily, rebalancing occurs only as needed when an asset class drifts far enough from its intended weighting in the portfolio to warrant a rebalancing trade. That typically results in a couple of rebalancing events per year in an average market environment. In a more volatile environment, the number of rebalancing events might be a bit higher, and in a very calm market environment it might be lower.”

5. Automatic withdrawals can come each month to your checking account.

Beginning January 2020, Schwab is starting a new service named Schwab Intelligent Income. Schwab Intelligent Income works in conjunction with Schwab Intelligent Portfolios to calculate a safe withdrawal rate and transfer that amount from your investments to your checking account each month. That gives you the money needed to live on each month, as if you were still earning a paycheck.

6. Charles Schwab is a massive company.

You should feel comfortable investing with Charles Schwab because it’s too big to fail. One of the lessons of the financial crisis was the fact that the government can’t let huge financial institutions go under. It causes too many job losses and destroys confidence. The entire system is held up on confidence, so letting banks fail is not something the government will do anymore.

7. Easy access to your account info.

With the Schwab Intelligent Portfolios, you can access your accounts any time and any place that you have internet access. You can get on the Internet and see your account performance or make additional withdrawals and contributions as the need arises.

The automation behind these intelligent portfolios makes it easy to manage your money as you get older and perhaps have less ability or interest in managing your accounts. The automation also means you do not need to pay a full-time financial advisor an AUM fee to manage these accounts.

You can hire Schwab Intelligent Portfolios do it for free and feel confident those savings are going to make your accounts last longer.

Premium Service (Extra Cost)

Schwab Intelligent Portfolios Premium is an additional service that offers access to one of Schwab’s advisors over the phone for $300 up front and then an ongoing $30 a month ($360 a year). According to the website, the advisor is a CERTIFIED FINANCIAL PLANNER™ professional.

However, because the Schwab advisor works for a broker, they are not a fiduciary and are not required to put your interest first. In fact, they are employed by Schwab, so their incentive is to make their bosses happy.

This premium service is a competitor of mine so obviously I would not recommend this paid, premium service.

You should get your investment advice from someone who will not profit from your decisions and who is required by law to put your interest first. That’s a fiduciary. I am a fiduciary as a Registered Investment Advisor with the State of California. I am also a CERTIFIED FINANCIAL PLANNER™ professional.

If you would like to talk about finding the best investment manager for your needs or other financial planning topics please schedule a meeting or phone call here.

Last week I attended the IMN Global Indexing and ETFs conference in Dana Point, California. One excellent benefit of living in North County San Diego is that many investment and financial planning conferences come to San Diego or Orange County. That makes it easy for me to attend.

I have been to this particular conference for four straight years now. In the past it has given me good insight into how the business behind ETFs actually works. This year, I learned about some funds that are worth a closer look. Those funds are: MOAT, ESPO, and IPAY. All three of these funds are thematic ETFs.

Thematic ETFs invest in companies that fit a certain story line. Having an investing story to tell increases the ability of the fund to gain assets. In other words, it’s easier for the fund to get some publicity, which leads to investors. If an ETF doesn’t attract enough investor money, it may not be profitable for the issuer, and they may decide to close it down. When investing, we want to make sure we are investing in funds that are large enough that they are not at risk of being shut down.

The downside of thematic ETFs is their investing story line may be too trendy and not have the staying power you need as a long term investor. Some examples of this are GNRX (a generic drug ETF), OBOR (China’s One Belt, One Road initiative ETF), or SLIM (an obesity ETF).

Let’s take a look at how the three thematic ETFs I learned about at the conference compare to some broad stock ETFs. We will compare against the old standard, SPY (S&P500 ETF), CAPE (an ETF that holds 4 sectors out of 9 based on value), and MTUM (a momentum smart beta ETF).

If you have read about Warren Buffet and his partner Charlie Munger, then you are familiar with the idea of companies having a moat. Their idea is to invest in companies that are able to protect their competitive advantage. They like it when it is difficult for a new company to easily replicate what the successful business is doing. An example would be Google. It would be very difficult for a new search engine to displace Google.

The MOAT ETF takes this idea and applies it based on Morningstar’s equity research. Morningstar determines which companies have a competitive advantage and buys the stocks with the lowest price to book value. If the price of the stocks increases and is no longer a good value, it is sold and replaced with another stock that meets the characteristics.

Overall, MOAT is an interesting idea, but I think it owns too many stocks with 52 currently. I think it would be a better investment if it toughened it’s definition of wide moat and invested in fewer companies. Also, just because a company is insulated from competitors, doesn’t mean people are interested in investing in it. These companies could just as easily be thought of as boring companies that don’t need to try hard or improve shareholder value.

The ESPO fund is the VanEck Vectors Video Gaming and Esports ETF. This ETF tracks an index of companies that get at least 50% of their revenues from video game development, Esports (including events), and related hardware and software.

What are Esports? Competitive video gaming. Esports have been a quickly growing industry the past few years. The performance of this ETF mirrors that.

I have seen Esports competitions broadcast on television. These broadcasts are of professional leagues featuring teams from around the world. Esports is a global industry and big events sell out huge arenas. It is definitely a growing industry. The question is will it continue to grow? My answer – most likely yes.

IPAY invests in companies that provide payment processing services, applications, and solutions, or provide software, networking or credit card processing. The companies must have a market cap of at least $500 million to enter the fund. There are many startups in this industry and the minimum market cap means the fund only invests in established companies.

The theme of this fund is the ongoing shift away from cash and towards mobile payments. Mobile payments is more than credit cards (although in my eyes a lot of these mobile solutions are really just software placed in front of credit card processing.)

The mobile payments industry is a lucrative and therefore competitive field. These businesses work by basically writing a piece of software that enables them to become middlemen and take a percentage of the mobile transactions that occur each day. It’s a huge market and you can see why there are lots of startups trying to create a technology that catches on.

Currently, there are a lot of competing technologies and none are revolutionary. I expect a lot of consolidation to occur in the coming years as some of the technologies become more established. The trend towards mobile payments should continue and therefore this thematic ETF should do well in the coming years.

Recent results chart: (For January 2016- May 2019. IPAY began trading in August 2015. ESPO began Nov. 2018.)

Ticker

Initial Balance

Final Balance

Avg Return

St Dev

Max drawdown

Sortino Ratio

US Mkt Correlation

IPAY

10000

18109

18.98

15.97

-17.97

1.75

0.88

MOAT

10000

16153

15.07

14.36

-10.34

1.53

0.91

MTUM

10000

15960

14.66

12.04

-15.44

1.73

0.86

CAPE

10000

15670

14.05

12.63

-15.27

1.55

0.96

SPY

10000

14392

11.24

11.8

-13.52

1.27

1

These returns are only for three years time because the thematic ETFs are new. The mobile payments ETF has had the best returns recently, but is also the most volatile. The standard deviation column shows IPAY is more than 4% more volatile each year than the S&P500 ETF (SPY). The MOAT ETF has had a better return with lower volatility than the S&P500. That is a small bit of evidence that the moat story line could be true.

How do Thematic ETFs fit in your portfolio?

Thematic ETFs should be used as a “satellite” to your core equity portfolio. You may get some extra return by adding a thematic ETF to your portfolio, if the story line holds up. The majority of your stock portfolio should be in a broad market fund, with the thematic fund(s) playing a bit role.

If you would like to talk about this investing idea or other financial planning topics, give us a call at (760) 651-6315.

Disclosure: Investing has risks. This blog post is not a recommendation to buy any of the mentioned funds. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed.

Financial planner vs financial advisor. What is the difference?

First, what is a financial advisor?

Your parents or your grandparents probably had a stock broker. Someone who suggested which shares of companies would be good investments. The stock broker was probably not investigating the companies he was recommending or doing any research himself. He was selling the shares his sales manager told him to sell.

Do you know anyone today who has a “stockbroker”? I only hear the term stockbroker when I am speaking with someone who is around 70 years old. If you do an online job search for stockbroker, you won’t get any results.Where did they all go?

The term stockbroker has been phased out as it began to take on bad connotations such as those portrayed in various movies and other pop culture. Think of the movies Wolf of Wall Street with Leonardo DiCaprio and Wall Street with Michael Douglas.

Nowadays stockbrokers are known as “registered reps” by those in the financial services industry. The registered rep. title comes from the regulatory body called FINRA (Financial Industry Regulatory Authority), which oversees these renamed stock brokers. They are registered representatives (salespeople) of the brokerage firm that they work for.

For those outside the financial services industry, stockbrokers are now called “financial advisors”. This is a bit confusing of course because there are other professionals who also use the term financial advisor. There are insurance salespeople, there are investment managers,fund salespeople, bankers, credit unions, tax preparers, mortgage brokers, real estate investors, and others. Financial advisor is a broadterm that can even include financial planners.

Generally speaking, a financial advisor makes money by selling insurance and/or investment funds for a commission. They are not required to put your interest ahead of their own.

What is a financial planner?

I define financial planner as someone who develops strategies to help clients maximize their financial future. The insurance and investment products necessary to implement that strategy are a secondary consideration. Planners plan. They don’t sell.

Financial planners don’t work for brokerage companies (also called broker/dealers). They work for registered investment advisors. That means they are regulated in a different manner from the registered representatives / stockbrokers / financial advisors mentioned earlier. The registered investment advisor regulations require planners to put their client’s interest ahead of their own. In other words, they are a fiduciary.

Is there a general rule of thumb?

If you want stand-alone investment advice, an insurance policy, or an annuity, then a financial advisor can provide you with those products.

If you want to coordinate various aspects of your finances, develop an integrated strategy or get help making a decision, then you want to see a financial planner.

How do you tell if someone is a financial planner or financial advisor?

The easiest way to check if someone is a broker is to look them up on FINRA broker check. https://brokercheck.finra.org/ You will need their name and city. If they come up on that search, then they are a broker and therefore a financial advisor.

I recently wrote a blog post about the best way to choose who you get your financial advice from is to understand their motivation. By motivation I mean understand how they are paid.

Businesses useconsultants to provide “objective advice and assistance relating to the strategy, structure, management and operations” of their organization. Consultants are paid to analyze the business, a project the business is considering (like expanding to new territory), or a situation it is in (such as selling a struggling division) and to make recommendations on how the business should proceed.

The business gets the benefit of the consultant’s expertise without committing to the ongoing relationship of hiring the consultant as a full-time employee.When the consultant’s project is complete, the two parties go their separate ways.

Did you know it is possible to hire a consultant foradvice and assistance with your personal finances?

Most people get advice froma financial advisor who is actually a salesperson of insurance, annuities, mutual funds, and other products. Or maybe they get advice from someone in related field like a CPA or lawyer who offer advice as a side business.

The best way to get personal financial advice; however, is from a financial advisor who functions as a consultant. You can hire a financial consultant to analyze any issue you are having with your finances. A majority of our clients hire Andrew Marshall Financial, LLC to objectively analyze their retirement readiness and create a plan for safely providing retirement income.

Financial advisors who practice in a consultant style are known as “fee-only” advisors.

Fee only advisors charge fees for their consultant work, they do not charge commissions. Fee only advisors often call themselves financial planners to distinguish themselves from commission based financial advisors.

The biggest benefit of hiring a consulting personal financial planner is the coalignment of goals between you and the consultant. A consultant will give you the best possible advice for your situation because they are not encumbered by the outside motivations of sales commissions.

Before hiring a financial advisor, determine what their motivation is. A financial advisor employed by an insurance company or investment company (like Merrill Lynch, Morgan Stanley, Fidelity, Vanguard, etc.) has sales managers above them who make sure the advisor is selling a certain number of contracts every month. You don’t want to be one of those sales targets. You want the advice of an objective consultant (fee only financial planner).

By hiring a financial planner as yourpersonal consultant, you will get an objective advisor who puts your best interest ahead of their own.

Before trying a new place or making a purchase, you probably look for online reviews on sites like Yelp, Amazon and Google. You have probably tried reading reviews of financial advisors and financial planners but it didn’t help much.

This is because financial advisors have not been allowed to post testimonials by their regulatory agency (SEC.gov). Most financial advisors have not posted client reviews in case the government considered reviews to be testimonials and reprimanded the advisor.

If online reviews aren’t helpful, how do you find a financial advisor you can trust?

By understanding the financial advisor’s motivation.

The most important thing to understand about a potential financial advisor or financial planner is how he / she is paid. Their method of compensation determines the advisor’s motivation.

There are conflicts of interest in the financial services industry that I have written about in the past. Each conflict of interest is a barrier to trust. Here are the possible ways an advisor gets compensated and the drawbacks of each.

1. Commissioned salesperson

Obviously, the method of compensation with the highest conflict of interest. Another name for this arrangement is “registered rep”. These advisors are affiliated with a broker. Not only do these people have the sales commission conflict of interest, but if they work for publicly traded companies (Morgan Stanley, UBS, Merrill Lynch, etc.) then there is another layer of conflict between the advisor and you.

Public companies have a goal of increasing profits every quarter and every year. The companies and employees are ultimately responsible to the shareholders. The way they increase profits is by taking it from their clients in the form of commissions and fees.

The multiple conflicts of interest in this model make trusting the advisor difficult.

2. Salaried salesperson

Slightly better than the first because the advisor is not getting commissions, but their livelihood still relies on meeting a quota each month. I will also include franchisees in this category. That means financial advisors who own Edward Jones offices for example.

3. Fee based financial advisor

This person charges in all manners possible. They take commissions for selling insurance and investments and may also charge fees for managing investments and fees for financial planning. They are probably really good marketers. They understand the obvious problems with number one and two above and have come up with a term that sounds like it is good for the customer, “fee based”, but in reality, it is a lot like one and two.

4. Fee Only Financial Advisor

This advisor does not take commissions. Fee only advisors are paid only by their clients. I would say being “fee only” is essential for finding a financial advisor you can trust.

It may seem like you are paying this type of advisor more than the others, but in reality, the amount has just been put out in the open. With the first three, the total amount of fees and charges you are paying is never revealed. That’s hard to trust.

5. Fiduciary

Fiduciary is a term that means the advisor will put your interests ahead of their own. A caring person would do that anyway, but there are laws to make sure that happens. If the advisor works for a Registered Investment Advisory (RIA) firm, then they are a fiduciary. They are required by law to do what is best for the client, not just what is “suitable”. If the advisor you are talking to is affiliated with a broker/ dealer or “dual registered” then you know they are not a fiduciary.

To find advisors in your area who are fee only and fiduciary, there are three websites you can use.

Being “independent” doesn’t carry as much significance as you might think. Financial advisors from all of the categories above except number 2 could call themselves independent. Independent in this case simply means they can recommend investments and / or insurance from more than one company.

Where does Andrew Marshall Financial, LLC fit?

Andrew Marshall Financial, LLC is a fee only (#4) and fiduciary (#5) financial advisor. We do not accept payment from any entity other than our clients. There are no hidden arrangements.

At Andrew Marshall Financial, LLC we go one step farther than even the vast majority of other fee-only advisors. We do not manage investments.

The conflict of interest between an advisor recommending you invest more, while simultaneously charging assets under management (AUM) fees has been removed from our financial planning services.

If you want to find a financial advisor you can trust, you must figure out how that advisor is being paid. They should be a fee only and fiduciary financial planner / advisor. The easiest way to find out is to read their website and ask them. If they won’t tell you up front, you should think twice about placing your trust in them. It doesn’t matter how nice a person they are when you meet them.

On my blog, one of the topics I like to cover is explaining how the personal financial advice industry works. Most people get financial advice from someone who is a salesman of insurance, annuities, mutual funds, and other products. You can also get help from someone whose main profession is something related like a CPA or lawyer who offer advice as a side business. The best way to get advice however, is from someone who functions as a consultant.

There are financial advisors out there that charge by the hour for financial advice. They often call themselves financial planners to distinguish themselves from financial advisors. You can find these financial planners through industry associations like the Garrett Planning Network and Fee Only Network.

I say it’s best to work with a consultant style of advisor because the consultant works only for you. Ask yourself what someone’s motivation is. A financial advisor employed by an insurance company or investment company (like Merrill Lynch, Morgan Stanley, Fidelity, Vanguard, etc.) has sales managers above them making sure they sell a certain number of contracts every month. You don’t want to be one of those sales targets. It may work out for you, and there are representatives who do look out for their clients, but ask yourself what their motivation is before signing anything.

By hiring a financial planner that charges fees only and no commissions, you are going to get an advisor who puts your best interest ahead of their own. Ask the advisor to sign the fiduciary oath. Advisors out to meet sales performance targets won’t put their fiduciary duty in writing. By going with a consultant style of advisor, not only will you get sound financial advice, you won’t wonder if the advisor recommended a product because his sales manager told him to.