A Roth Conversion Case Study

I worked with a recently retired couple with a very strong financial position.

They wanted to spend approximately $140,000 per year in retirement. They hoped they could afford to spend $160,000 per year for a very comfortable lifestyle, including more travel.

After completing their retirement plan, they learned they could safely afford to spend approximately $230,000 per year.

That difference matters.

They had $70,000 per year of additional spending capacity beyond the amount needed for a very satisfying retirement lifestyle. That gave them the ability to pay Roth conversion taxes without reducing their desired retirement spending or creating a meaningful risk of running out of money.

This is a key feature of a strong Roth conversion opportunity.

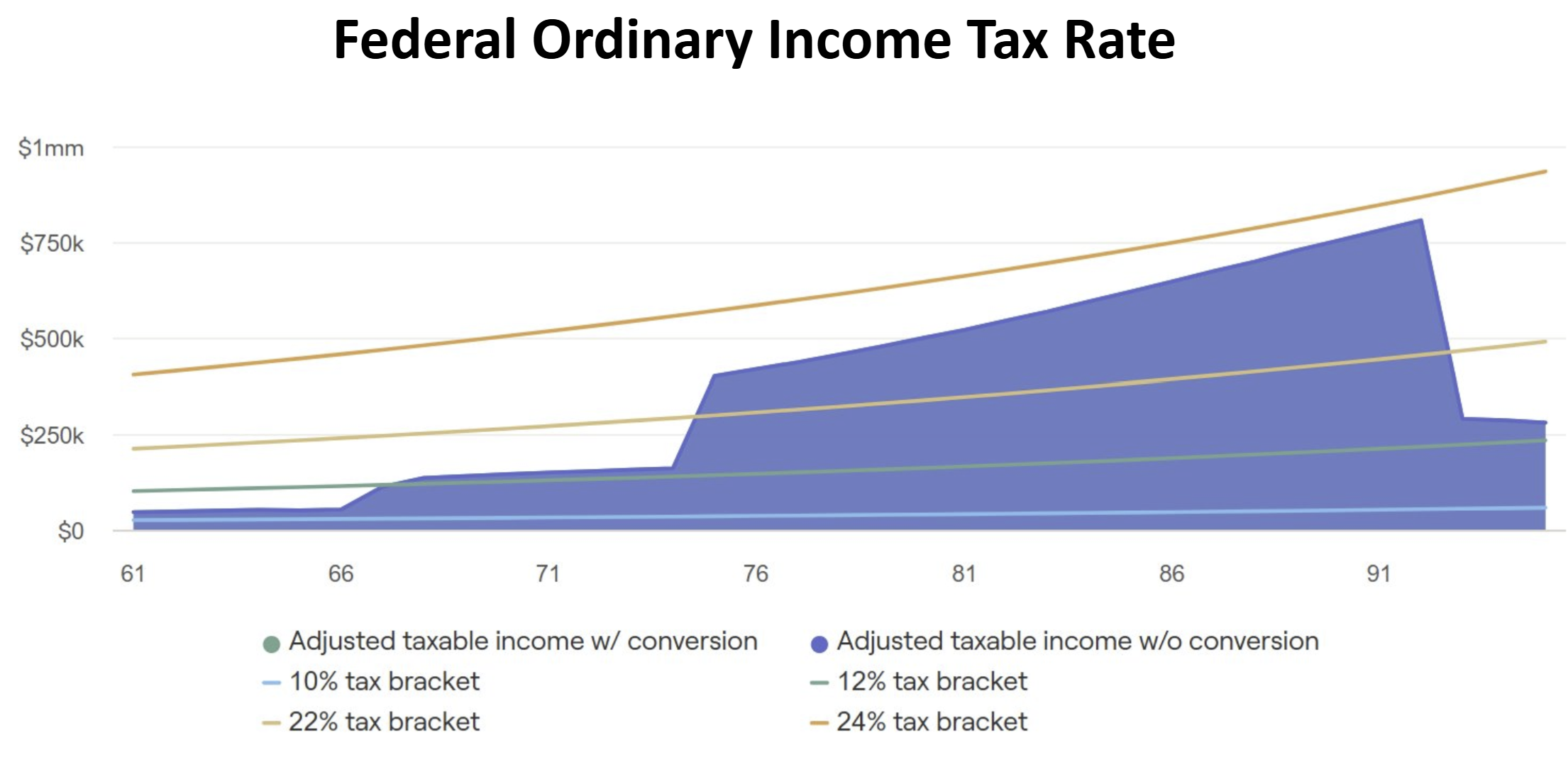

The following diagram shows their taxable income by year in the blue-shaded area.

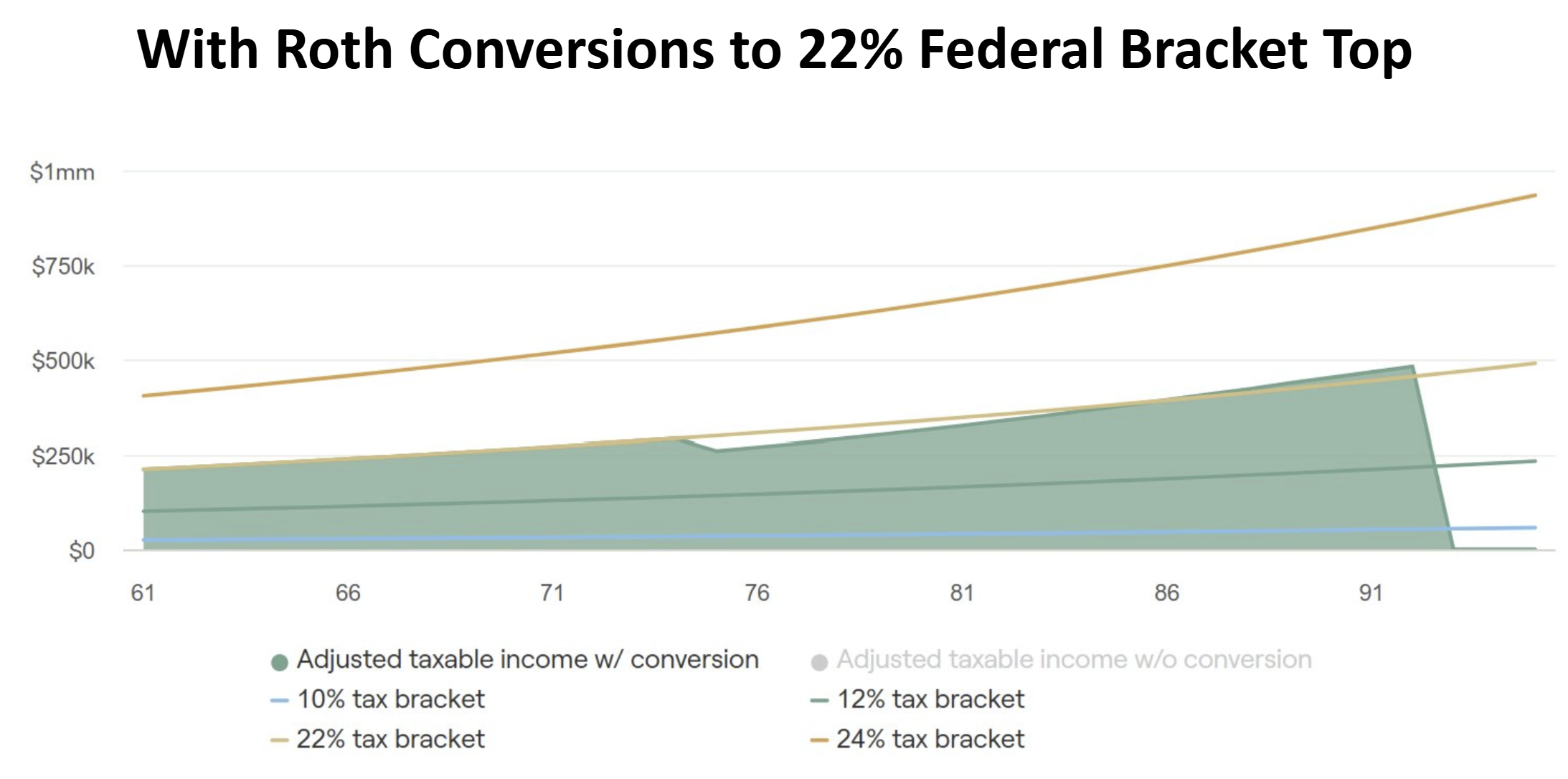

Filling Up the 22% Federal Tax Bracket

For this couple, the strategy was to complete annual Roth conversions up to the top of the 22% federal income-tax bracket.

This increased their taxable income during the first 14 or so years of retirement. However, it substantially reduced taxable income later in life.

Rather than allowing their future RMDs to force them into higher tax brackets, they deliberately used lower-tax years to move money from traditional retirement accounts into Roth IRAs.

Under the assumptions used in their retirement plan, the couple would remain mostly within the 22% federal tax bracket for the rest of their lives. They might move slightly above that bracket in their 90s, but not nearly as much as they would without Roth conversions.

Tax laws and tax rates can change, of course. Any Roth conversion analysis must use current law while also recognizing that future tax policy is uncertain.

After conversions, their taxable income by year is shown in the green-shaded area.

The Potential Benefits of Roth Conversions

For this particular couple, the Roth conversion strategy created significant long-term benefits.

More After-Tax Wealth for Their Children

The projected result was more than $1.9 million in additional after-tax ending portfolio value.

This matters because children and other heirs who inherit traditional IRAs or 401(k)s must empty the accounts and pay income taxes within 10 years. Inherited Roth IRA are much more tax-efficient.

For this couple, Roth conversions were not simply about reducing their own future taxes. They were also about improving the after-tax inheritance available to their children.

Lower Lifetime Taxes

The projection also showed approximately $954,000 less in lifetime taxes.

That does not mean every dollar converted avoided taxes. The couple still paid tax on the Roth conversions. But they paid those taxes during years when their marginal tax rate was lower than it was expected to be later.

The goal of Roth conversions is often to pay tax at a lower rate today, rather than being forced to pay tax at a higher rate later.

Lower Required Minimum Distributions

Their projected RMDs would be more than $2.6 million lower over their lifetime.

Reducing RMDs can create several advantages:

- Lower taxable income in later retirement

- More control over annual income

- Less chance of being pushed into higher tax brackets

- Lower exposure to Medicare IRMAA surcharges

- More flexibility for charitable giving and estate planning

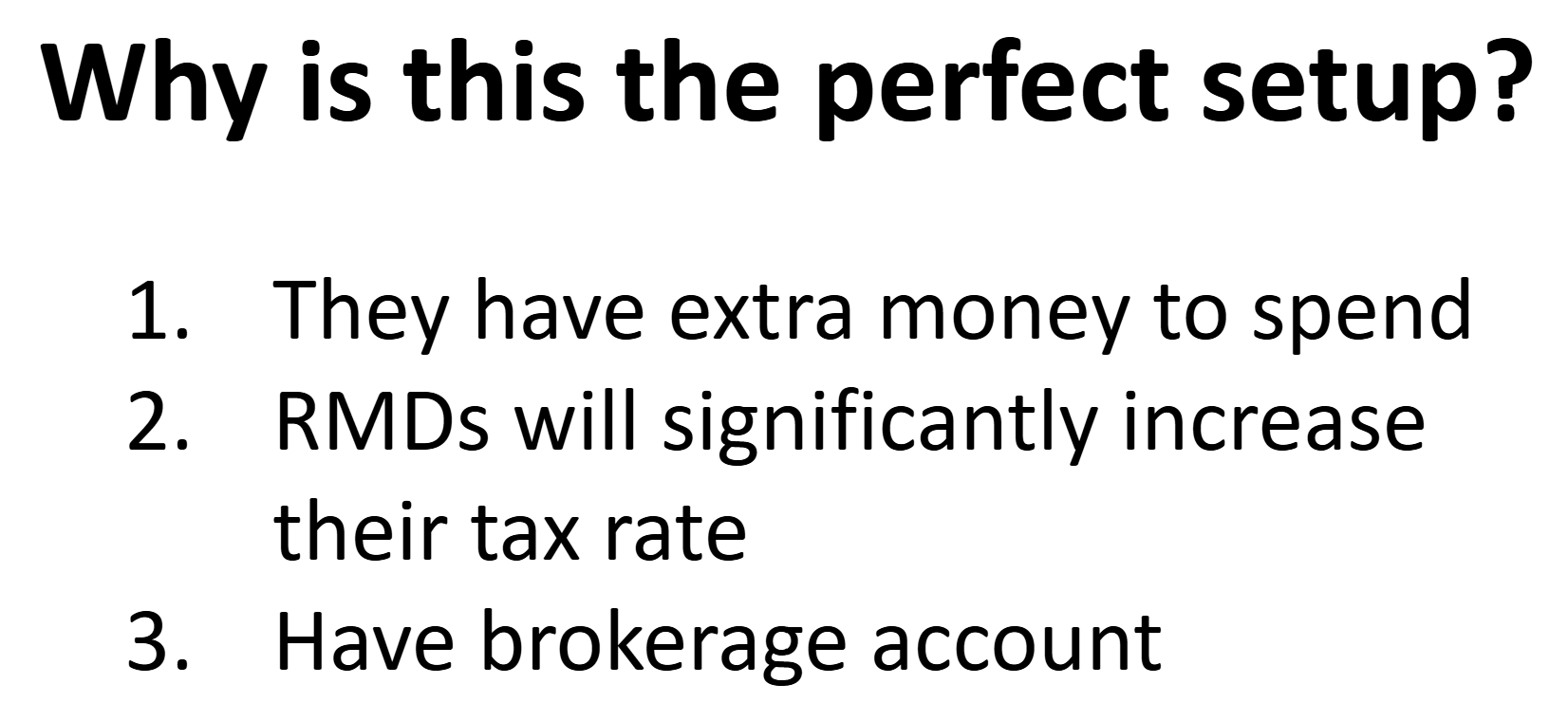

Why This Couple Was an Ideal Roth Conversion Candidate

This couple had three qualities that made Roth conversions especially attractive.

1. They Could Afford the Taxes

This was the most important factor.

They hoped to spend about $160,000 per year to enjoy retirement. Their financial plan showed that they could safely spend about $230,000 per year.

That gave them approximately $70,000 per year that could potentially be used for Roth conversion taxes without reducing their lifestyle or undermining their financial security.

Many retirees do not have this flexibility. They may need most of their available income to fund normal living expenses. In that situation, large Roth conversions may create unnecessary pressure on cash flow.

2. Their Future RMDs Were Expected to Be Large

Large traditional IRA and 401(k) balances can create a future tax problem.

Retirees who delay withdrawals from large tax-deferred accounts may eventually face substantial RMDs. Those withdrawals can occur at the same time Social Security benefits, pensions, investment income, and rental income are already increasing taxable income.

If future RMDs do not push one into a much higher bracket, then paying taxes up-front in retirement for Roth conversions may not make sense.

3. They Had a Taxable Brokerage Account

The couple had a brokerage account that could be used to pay the income taxes generated by Roth conversions.

This is important.

Using taxable brokerage assets, cash reserves, or other non-retirement funds to pay conversion taxes generally allows more money to remain inside the Roth IRA, where it can potentially grow tax-free.

If someone must withdraw part of the converted IRA money to pay the taxes, the strategy becomes less attractive.

The Bottom Line

Roth conversions can be an excellent retirement tax-planning strategy. But they are not universally beneficial.

They often work best for retirees who have:

- Ability to afford paying taxes voluntarily

- Significant IRA and 401(k) balances

- Lower-income years immediately after retirement

- Large projected future RMDs

- Taxable brokerage assets or cash available to pay conversion taxes

- A desire to leave more after-tax wealth to children or other heirs

For the right household, Roth conversions can lower lifetime taxes, reduce required minimum distributions, and create substantially more after-tax wealth.

For everyone else, the benefit is not worth the cost.