With summer approaching, now is a good time to compile a list of the top vacation destinations for the Summer of 2017. This list is unlike any other, however. Rather than finding you the hip and trendy places being promoted by tourism bureaus, our destinations give you bang for your buck. We ranked these destinations by how much cheaper they are this year, compared to last year, based on the US dollar exchange rate.

The US dollar has been getting stronger over the past few years. This is a great thing for American travelers going abroad. Other currencies have been struggling, like the British pound, after the Brexit issue. This creates opportunities for Americans because when we exchange our dollars, we get more of the local currency in return. This leads to a cheaper vacation.

Here are the top destinations:

Exchange rate percentage change for 1 USD between April 30, 2016 and April 19, 2017.

These rankings tell us a trip to Britain, Scandinavia or Eastern Europe would be the best value this summer. Alternatively, both Canada and Mexico offer good alternatives if you want to stay closer to home.

Those of you who want to go to Europe (all Euro currency countries) will be happy to know that Europe is 5.9% cheaper than last year. It would be a good value to go to Europe and combine those countries with Scandinavia or Eastern Europe.

Will your Social Security payments cover your retirement lifestyle? Do you plan to rely on Social Security for most of your retirement income?

Most people have no idea how their future social security payments compare with their current income. If you are thinking you can retire in five years or less, make sure you log on to ssa.gov and look at your Statement. Your Statement will give you an estimated monthly benefit payment that you have accumulated. This is what you would get if you retired tomorrow. Is it as much as you were expecting?

I doubt it. I find people vastly underestimate the amount of money they will get from Social Security. This can have a dramatic effect if you are approaching retirement and expecting a larger amount than you are due. If you are counting on Social Security to provide a large portion of your retirement income, think again.

Social Security was designed as a safety net to provide the poorest Americans with food and shelter in their old age. Social Security is not an income replacement program or a retirement plan for the masses. It is an anti-poverty program. Those who have middle to high incomes will not receive anywhere near their current income from Social Security.

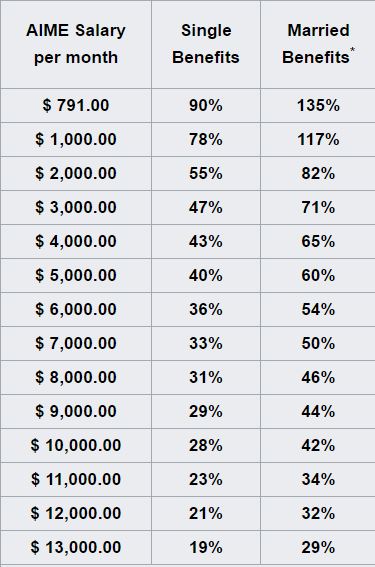

The chart at left shows the average indexed monthly salary (AIME) and the corresponding percentage of that salary that will be received from social security. The average indexed monthly salary takes your highest 35 years of salary and indexes each year for inflation so that your early years of work are given the same weight as recent years. That doesn’t mean you can look at the chart and see what you are making now and look to see the percentage.

Most people’s salary has progressed over their career, but some people have low or non-earning years if they left the workforce to raise kids for example. These lower year’s decrease your average. In order to get an estimate on what your average is, you have to go online to My Social Security.

Let’s look more closely at the chart numbers again and examine two scenarios. Someone who has had a good paying job and has an AIME of $8,000 per month (about $100,000) per year will have a payment of 31%. That’s 31% of 8,000 per month. Or $2,480. If this person is relying on Social Security to cover their retirement expenses, they are in for a challenge. It is really hard to change your lifestyle from living on $8,000 per month to $2,480!

I mentioned earlier that Social Security is really a program to keep people out of poverty. The poverty level for a single person is $11,880 per year. Let’s call it $1,000 per month. Someone earning $1,000 per month would receive $780 per month from Social Security. Now it would be hard to live on that amount, but it would not be as big of a change from $1,000 to $780 per month as the change would be from $8,000 to $2,480.

This issue of Social Security payments being smaller than expected is one of many reasons it is a good idea to talk to a fee only financial planner as early as possible. By monitoring your financial situation and working with a fee-only financial planner for many years leading up to retirement, low Social Security payments won’t come as a shock.

To retire comfortably, you need other sources of income. It is important to work somewhere that provides a pension, 401(k) or other retirement savings, so you are forced to contribute before it is too late. If there are no other retirement savings, then there may be no choice for retirement other than working longer and experiencing a major lifestyle change. Neither of which are much fun.

Social Security Survivors benefits are paid to widows, children, parents and ex-spouses of covered workers.

The Social Security program actually consists of three benefit programs that make payments for various reasons. They are:

Retirement benefits,

Disability benefits,

Survivors benefits.

This post covers number 3, Survivors benefits. These are not the same as the benefits commonly referred to as spousal benefits.

If a worker, who is covered by Social Security, dies and leaves family members behind, they are the “survivors” and are covered under the Survivors benefits program. Social Security will use the deceased worker’s record to calculate payments for his / her family.

There are four eligible parties that may receive payments after the worker’s death. They are the widow (or widower if the wife dies first), children, parent, and ex-spouse. Each has detailed rules for eligibility.

A widow(er) will get benefit payments if:

They are age 60+, or

Age 50+ and disabled, or

Any age and caring for a worker’s child under 16 or disabled and entitled to benefits on worker’s record.

A child will get benefit payments if:

They are under age 18, or

Between 18 and 19 and still in secondary school, or

Over age 18 and severely disabled before age 22.

A parent will get benefit payments if:

They are dependent on the deceased worker for greater than 50% of their support

An ex-spouse will get benefit payments if:

They fit one of the three requirements for widow(er) above and were married to covered worker for 10 or more years, and

They are not entitled to a larger benefit based on their own record, and

Not currently married unless marriage was after they turned 60 or 50 and are disabled.

Another aspect of Survivors benefits that comes into the payment amount is that the “full retirement age” (FRA) for Survivors benefits is different from the full retirement age for retirement benefits.

Birth Year

Survivors FRA

Retirement FRA

1937 or earlier

65

65

1938

65

65 and 2 months

1939

65

65 and 4 months

1940

65 and 2 months

65 and 6 months

1941

65 and 4 months

65 and 8 months

1942

65 and 6 months

65 and 10 months

1943

65 and 8 months

66

1944

65 and 10 months

66

1945-54

66

66

1955

66

66 and 2 months

1956

66

66 and 4 months

1957

66 and 2 months

66 and 6 months

1958

66 and 4 months

66 and 8 months

1959

66 and 6 months

66 and 10 months

1960

66 and 8 months

67

1961

66 and 10 months

67

1962 or later

67

67

This chart matters because a widow(er) or ex-spouse can start claiming benefits as early as age 60, but the benefit will be reduced. For the full benefit payment, the survivor must wait until their FRA in the center column above. For some people it is several months earlier than the full retirement age for Retirement benefits and they may wait unnecessarily long to receive their benefits if they are unaware of this anomaly in the Social Security benefits.

Health Savings Accounts (HSA) are a smart way to establish an extra source of funds you can tap into to cover medical expenses later in life. You can use the funds immediately, but the true benefit comes after giving the account a chance to grow. HSAs are accounts, held by a custodian such as a bank, whose withdrawals (including the gains from investing the savings) are tax free if used for health care expenses. By taking advantage of these accounts, the government hopes citizens will be better able to cover the future costs of health care. We all know medical costs are increasing quickly, and we have heard the stories about people who are forced to spend down all or most of their retirement savings to cover their health care costs. A health savings account should provide you with an extra layer of protection in the future.

First question is, who is eligible for an HSA? 1. You cannot be claimed as a dependent on someone else’s tax return. If they could claim you but don’t, then you are not eligible. 2. You cannot be on Medicare. 3. You must be covered by a High Deductible Health Plan (HDHP) and no other plan on the first day of the month. (There are of course exceptions, but these are mostly for additional plans that do not pay before the HDHP deductible is reached.)

Second question is how much can someone contribute to their HSA in 2016? The contribution limits for 2016 are $3,350 for someone with self-only HDHP coverage and for a family with HDHP coverage the max is $6,750. These amounts are the maximum for someone with qualifying health insurance and HSA eligibility each and every month of the year. Some people aren’t eligible every month of the year, and they need to do a calculation to determine how much their maximum is. Contributing more than your maximum allowed and not correcting the mistake will lead to a 6% excise penalty.

Additional Contribution: Those eligible individuals who are 55 years of age and older at the end of their tax year are allowed to contribute an extra $1,000.

The last-month rule is a shortcut determination used to determine if you are eligible to contribute the maximum amount. The last-month rule states that a person who is eligible to contribute to an HSA on the first day of the last month of their tax year is treated as being eligible the entire year. The day used for determination is December 1 for most people. So if you meet the requirements on December 1, you can contribute $3,350 for a single person or $6,750 for a family.

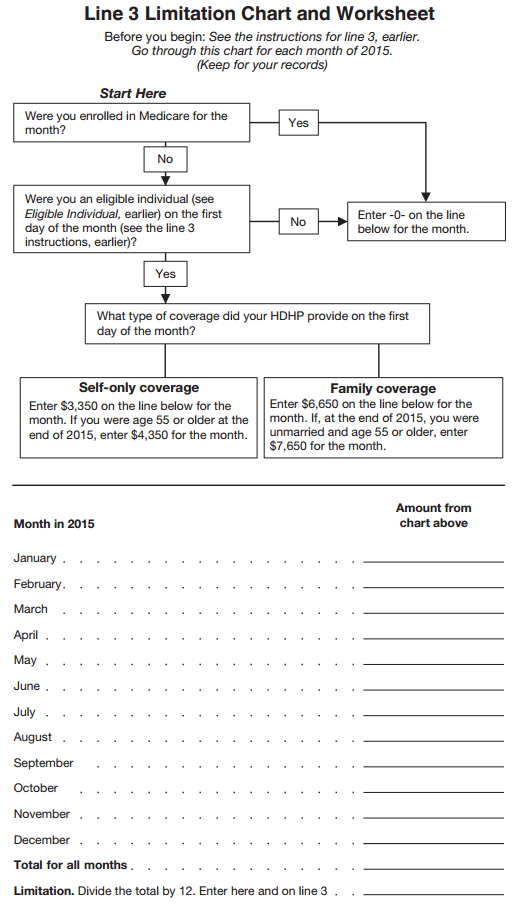

What if I wasn’t covered in the last-month? You must use the “Line 3 Limitation Chart and Worksheet” found in the instructions pdf for IRS Form 8889.

Putting money away in a Health Savings Account is a good idea if you are eligible for one. Many employers are now offering it as an alternative to HMO medical coverage. Be sure to calculate your maximum allowed to avoid paying penalties.

Yesterday I answered a press request asking about when is the best time to start saving for retirement. The standard answer is as early as possible. This comes from the idea that having more years to compound your returns will lead to a bigger account. I argue it’s the years at the end that are more important than the early years.

First let’s review the power of compounding. When you invest money and earn a return, your account is worth more at the end of the year. In the second year, you earn return on a larger amount than the first year because your beginning balance in year two is the original year one principal plus the year one return earned. Each successive year will see larger gains as return is earned on a larger starting amount. The account will continue to grow even without new additions.

When young people finish school and start working around age 22, they usually are not making a significant salary. This leaves them little extra money available for saving. If someone starts with saving $100 per month or $1200 per year, and earns 7%, then how much will they have after five years? My financial calculator tells me it’s $6,900.

This person did the “right thing” and started early in their retirement savings. I would argue that saving this much by age 27 is not crucial to retirement. A large contribution in year six can easily make up for the first five years. It’s not necessarily how early you start, but a combination of how much is saved and for how many years.

Now we look at return at the beginning of the 30 year time frame versus at the end. When this example person is 28 years old and in year six of compounding, a 7% return on the $6900 they struggled to accumulate over five years will return $483. At the end of the compounding years however, when the account value is say $1,000,000, then he/she will make $70,000 return in one year. Just one additional year at the end brings another $70,000 versus $483 at the beginning.

As this person progresses in their career, they will receive pay raises and move up the corporate ladder. Using these pay raises wisely will have a more significant impact on their retirement than saving as early as possible. Staying invested at 7% for three additional years at the end of their career will turn a $1,000,000 portfolio into a $1,225,043. Twenty-two percent more savings for retirement. See the importance of the later years?